Products You May Like

Executive Summary

Taxes and their broader impact are generally overlooked in American education. Taxes influence earnings, budgets, voting, and decisions on where to live, but do American taxpayers understand the US taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

system?

In 2024, the Tax Foundation’s educational program, TaxEDU, and Center for Federal Tax Policy conducted a poll with Public Policy Polling (PPP) to gauge Americans’ knowledge of basic tax concepts and opinions of the current tax code. The results indicate that most Americans are confused by and dissatisfied with the federal tax code.

Our objective in this report is to delve further into the survey results to assess how individuals from various demographic backgrounds perceive the US tax system and understand key tax-related concepts. Additionally, we explore how different levels of tax knowledge influence views of the tax system and whether an understanding of one aspect of tax literacy correlates with comprehension of related tax perspectives. This analysis allows us to identify the key demographic and knowledge-based factors that primarily influence tax perception and literacy, providing deeper insights into how various populations engage with the US tax system.

The National Tax Literacy Poll highlights the need for and importance of tax education for everyone, as most Americans of all ages, incomes, education levels, and political affiliations misunderstand taxes and are dissatisfied with the tax code. As the US continues to focus on financial literacy in education, these results can guide educators’ efforts.

Key Findings

- The majority of respondents do not know or were not sure of basic tax concepts related to income tax filing.

- Higher proficiency in tax literacy correlates with higher earnings and higher educational attainment.

- Individuals with “proficient” tax knowledge are more likely to understand and correctly identify basic tax concepts and align their perceptions with tax planning best practices.

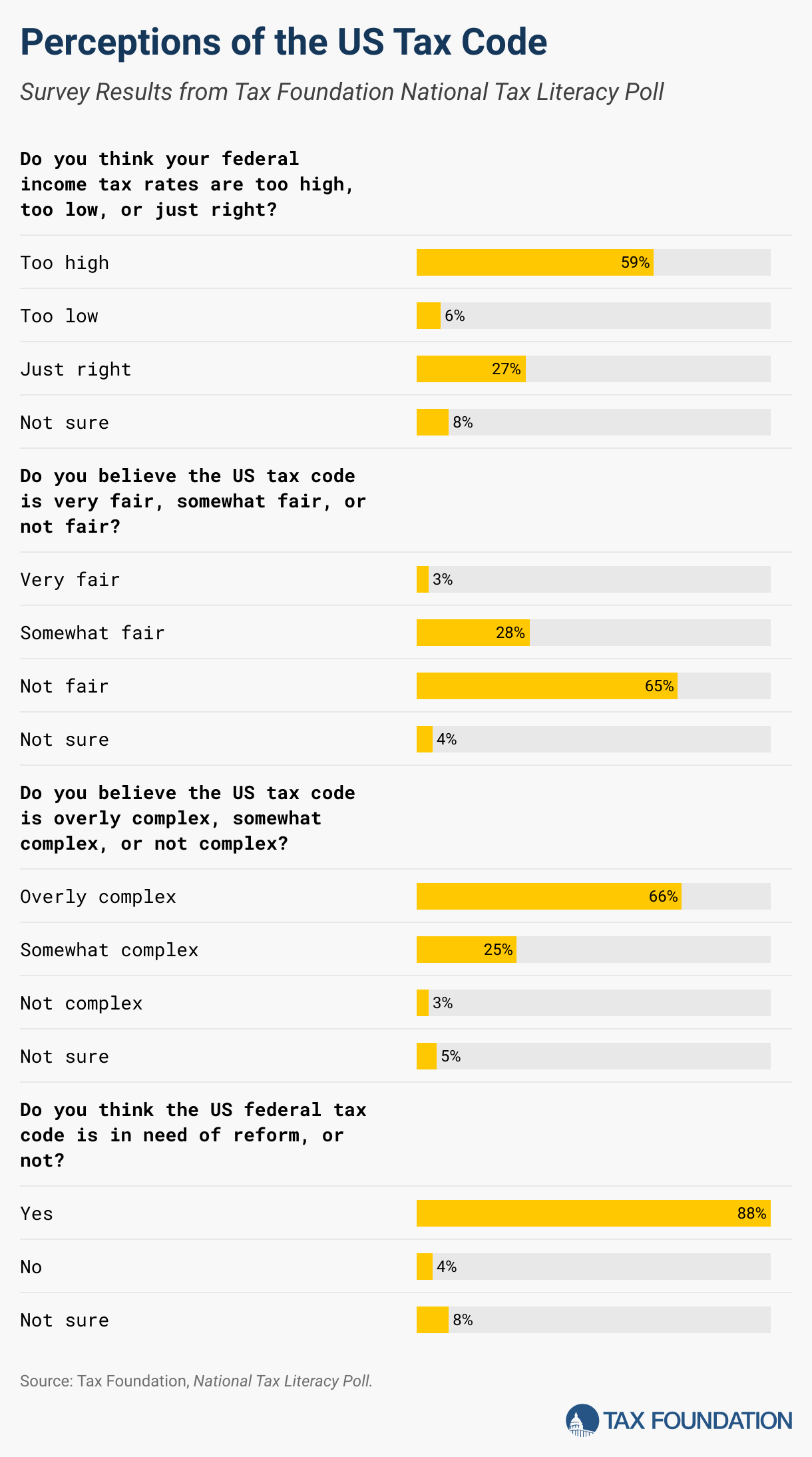

- More than 80 percent of respondents think the US federal tax code needs reform.

- More than half of respondents think federal income taxes are too high.

- Sixty-five percent of respondents think the US tax code is not fair.

Background

Tax Foundation conducted this survey to gauge American taxpayers’ tax literacy and their perceptions of the current tax code to better understand the general public’s need for tax education.

More than half of US states have mandated or are in the process of implementing financial literacy education requirements in high schools. As these courses develop, tax literacy should be a key component, giving students a complete picture of earnings, budgeting, saving, and investing by teaching about taxes. This movement was another factor in the execution of Tax Foundation’s National Tax Literacy Poll.

Consumer Misconceptions about Tax Laws: Results from a Survey in the United States, published in May 2020, surveyed US consumers on their knowledge of “fundamental US tax law concepts,” like withholdingWithholding is the income an employer takes out of an employee’s paycheck and remits to the federal, state, and/or local government. It is calculated based on the amount of income earned, the taxpayer’s filing status, the number of allowances claimed, and any additional amount of the employee requests.

, tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat.

, and payroll taxes. This survey also identified a low literacy level (30 percent to 79 percent) for basic tax concepts related to tax filing.

Measuring Tax Literacy in a Politically Charged Climate, a survey conducted in October 2023 by Texas Law Review, also explored tax literacy and tax perception. The survey had comparable results but focused more directly on political affiliation when analyzing tax literacy. Another similar tax literacy survey was conducted in 2009 by H&R Block, but financial education requirements, social media, and the political landscape have changed drastically in 15 years.

Other surveys focused on people’s perceptions or understanding of the tax code tend to focus on more narrow tax policy areas, such as regressive taxes, tax brackets, or survey-specific groups like small business owners.

Over 162 million individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S.

returns were processed by the IRS in 2023, representing the vast majority of US households. Taxes play a critical role in the lives of individuals and families, and tax literacy can impact financial planning, job opportunities, where someone lives, and how they vote, among other decisions.

Tax Foundation exists as an educational organization focused on improving lives through sound tax policy. To best tackle a tax literacy gap in the US, we first must understand the problem.

Methodology

This report draws on data from the National Tax Literacy Poll, conducted in collaboration with Public Policy Polling (PPP), to examine knowledge of and opinions about the tax code among US taxpayers. The initial dataset comprised responses from 2,767 individuals. PPP applied filtering and random iterative method (RIM) weighting techniques to align the sample more closely with the actual population, adjusting for variables such as age, gender, party affiliation, race, and income level. Our previous posts in April and May were based on PPP’s preliminary analysis.

For this report, we adopted a distinct approach to ensure transparency, consistency, and clarity of findings. We refined the dataset to focus exclusively on respondents who completed all 28 survey questions, resulting in a final sample size of 2,064 respondents. While PPP’s methodology involved applying RIM weighting to align the sample with the broader population, we opted to analyze the unweighted data. By analyzing the unweighted data, we aim to offer a different perspective that provides a clear and direct interpretation of the raw responses.

To assess the reliability of this alternative approach, we conducted a comparative analysis between our filtered dataset and the original PPP weighted dataset. Although some variations were observed in the distribution of responses to certain survey questions, the overall patterns across most questions remained consistent. These findings suggest that our methodology provides a reliable basis for analysis while offering a different yet valuable perspective on the data.

This report is structured into two primary analytical sections that were in the survey: tax perception and tax literacy. Additionally, we examine how varying levels of tax literacy influence respondents’ perceptions of the tax system and tax policy.

To facilitate our analysis, we created dummy variables for key areas of interest: TaxLiteracyLevel, EducationCategory, and Within22TaxBracket. We then conducted cross-tabulations between these demographic variables and both the tax literacy and perception questions. Additionally, Chi-square tests were performed to evaluate the statistical significance of relationships within the tax literacy questions and between demographic factors and tax literacy.

Our objective is to assess how individuals from various demographic backgrounds perceive the US tax system and understand key tax-related concepts. Additionally, we explore how different levels of tax knowledge influence views of the tax system and whether an understanding of one aspect of tax literacy correlates with comprehension of other tax-related perspectives. This analysis allows us to identify the key demographic and knowledge-based factors that primarily influence tax perception and literacy, providing deeper insights into how various populations engage with the US tax system.

Section A: Tax Literacy Analysis

Main Takeaways

- Regardless of educational attainment, more than half of the respondents lack basic tax literacy.

- Higher education levels are generally associated with better performance on tax knowledge questions.

- Younger and middle-aged respondents (18-45) and respondents with higher household incomes ($100,000 and above) generally perform better on tax knowledge questions.

- Income levels influence financial literacy via perceptions of tax refunds: over half of respondents with incomes over $50,000 disagree that large tax refunds are beneficial, while only one-third of lower-income respondents shared this view.

- Only 2 percent of respondents exhibit “proficient” tax knowledge.

Analytical Approach

To assess tax literacy, we focused on survey questions 14 through 18, which were specifically designed to evaluate respondents’ knowledge of key tax concepts. We excluded question 19 from the tax literacy categorization as it reflects opinions rather than objective tax knowledge. However, question 19 is included in this section to explore respondents’ perspectives on tax refunds in relation to tax proficiency.

For the analysis, we first created dummy variables :

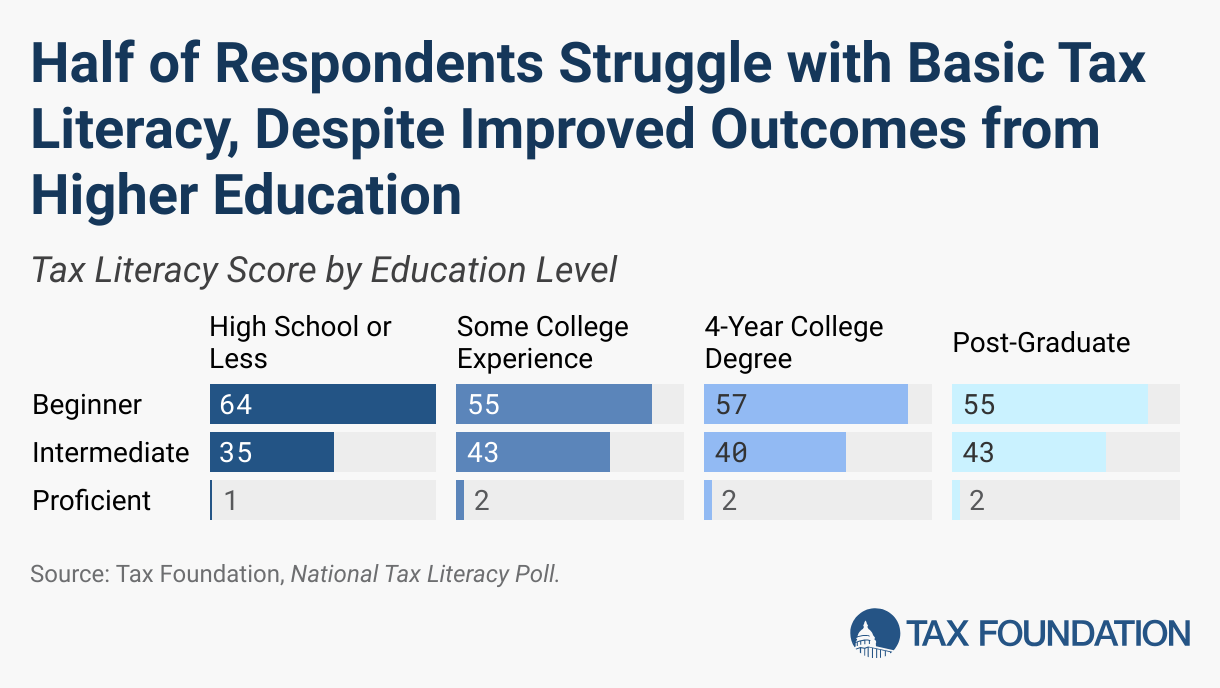

- TaxLiteracyLevel: This variable categorizes respondents based on their overall tax literacy, as determined by the number of correct answers to questions 14-18. The levels are defined as “beginner” (0-1 correct answers), “intermediate” (2-3 correct answers), and “proficient” (4-5 correct answers).

- EducationCategory: This variable recategorizes respondents’ educational levels into four groups: high school or less, some college experience, four-year college degree, and post-graduate education.

Then, we conducted cross-tabulations to explore the relationships between respondents’ tax literacy and various demographic factors. Finally, to assess the statistical significance of these relationships, we performed Chi-square tests. This allowed us to determine whether the observed associations between demographic factors and tax literacy were likely due to chance or represented meaningful patterns in the data.

Analysis

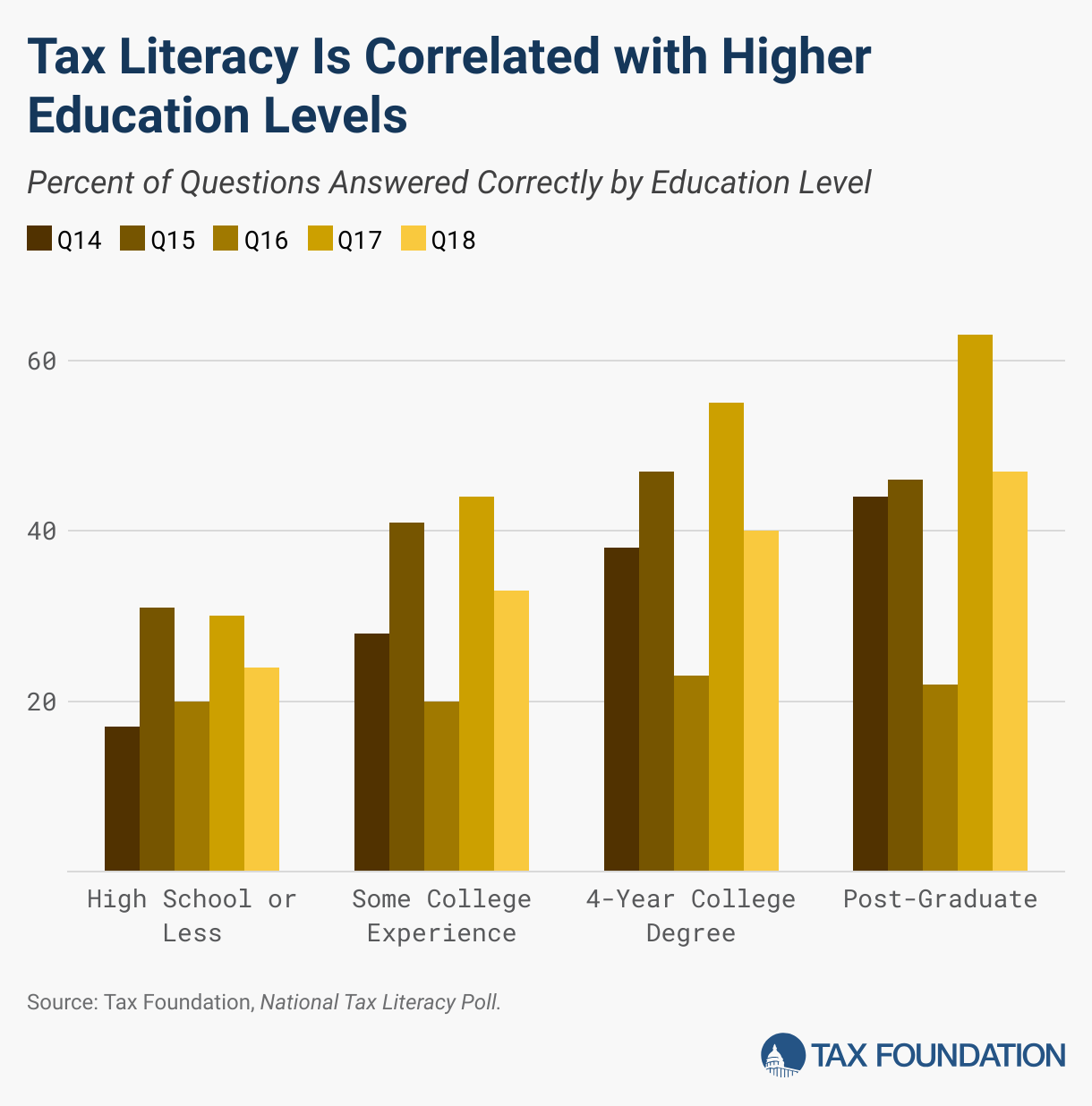

Education Level and Tax Literacy

The educational distribution of the respondents suggests that the sample is relatively well-educated: only 11 percent of participants are in the high school or less category, while 32 percent have some college experience, 29 percent have completed a four-year college degree, and 28 percent hold a post-graduate degree.

Understanding of the current (2023) top federal income tax bracket improved with higher education levels, and the analysis reveals a significant correlation between education level and tax literacy across most tax knowledge questions. However, tax literacy was not high among any education group, as was the case with most demographic variables in the survey. While higher education is generally associated with better performance on individual tax literacy questions, the overall distribution of TaxLiteracyLevel, categorized as beginner (57 percent), intermediate (42 percent), and proficient (1.99 percent)—shows a somewhat different pattern. When we categorized respondents based on the number of correct answers across five tax literacy questions, we observed that a significant portion of respondents in each education group still fell into the beginner category. Sixty-four percent of those with a high school education or less, 55 percent of those with some college experience, 57 percent of those with a four-year college degree, and 55 percent of post-graduates are categorized as beginners.

Despite this, education level does have a significant impact on tax literacy outcomes. As educational attainment increases, the proportion of respondents in the beginner category decreases, while the percentage of intermediates rises. For example, the proportion of respondents categorized as intermediates increases from 35 percent among those with a high school education to approximately 43 percent among post-graduates. However, the proportion of respondents categorized as “proficient” remains relatively small across all educational levels, with only 0.90 percent of those with a high school education or less demonstrating “proficient” tax knowledge. This percentage increases slightly with higher education: 2.26 percent for those with some college experience, 2.18 percent for those holding a four-year college degree, and 1.89 percent for those with post-graduate education.

Respondents with higher education levels generally displayed better understanding and fewer misconceptions. For example, understanding of the current (2023) top federal income tax bracket (Q14) improved markedly with higher education, with about 40 percent of respondents with four-year college experience or a higher degree answering correctly, compared to just 17 percent of those with a high school education or less.

Additionally, the ability to correctly answer questions related to the value of tax deductions versus tax credits (Q18) also improved with education. Nearly double the respondents with post-graduate education answered correctly compared to those with only a high school education (47 percent vs. 24 percent).

However, the complexity of certain tax concepts can still lead to misconceptions, even among those with higher education. This is particularly evident in question 16, which asks about the tax burden on the top 1 percent of taxpayers. Only 22 percent of respondents answered correctly, and misconceptions about the taxation of the wealthy are pervasive across all education levels.

These findings suggest that while higher education improves the likelihood of achieving a moderate level of tax literacy, a significant portion of even the most educated respondents struggle to reach a “proficient” level. This highlights the need for more targeted tax education efforts to bridge the gap in tax literacy across all educational levels.

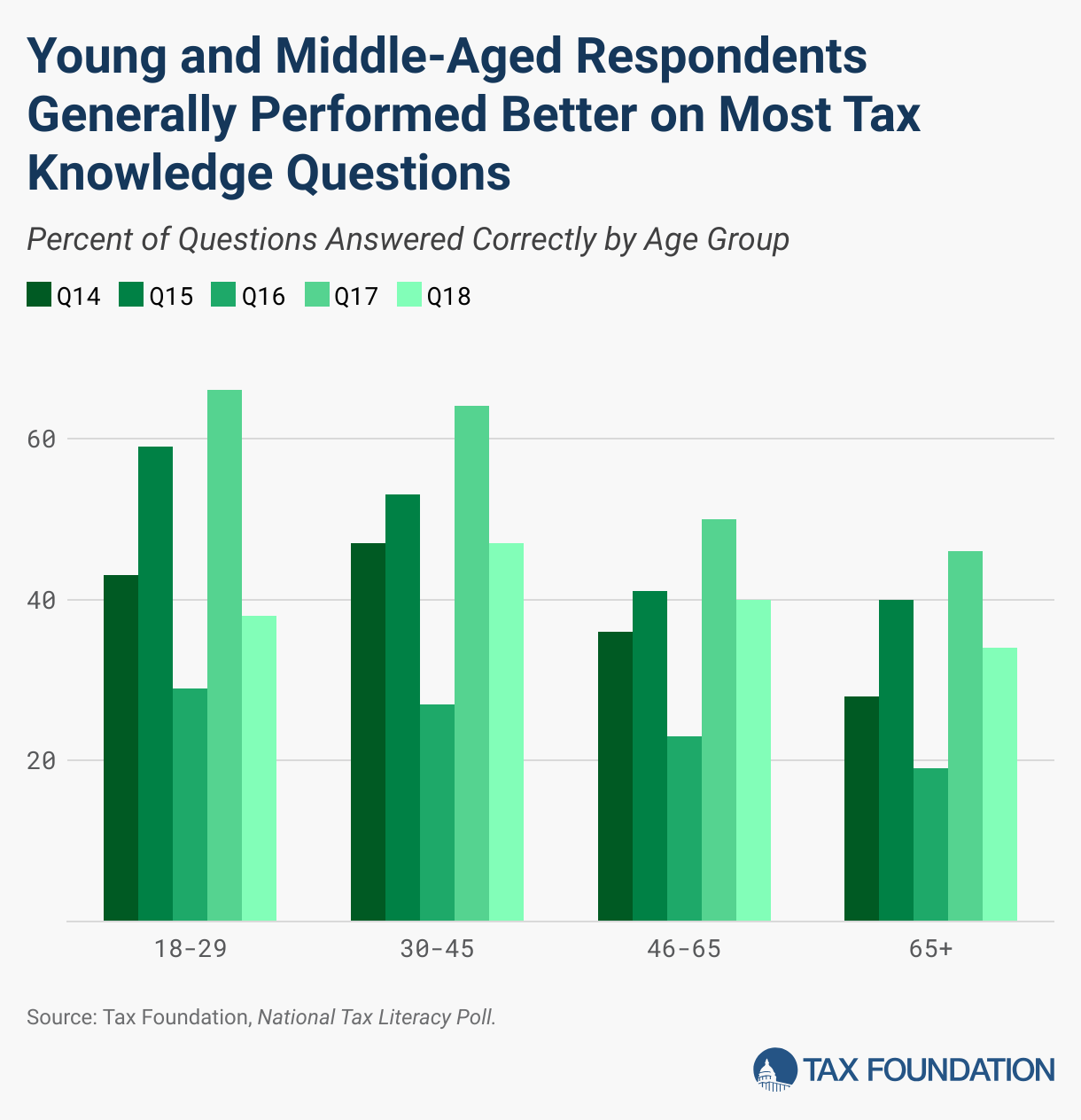

Age and Tax Literacy

Age also plays an interesting role in tax literacy, with younger and middle-aged respondents (18-45) generally performing better on most tax knowledge questions compared to older age groups.

For instance, about 55 percent of respondents aged 18-45 correctly identified the average federal income tax rate (Q15), compared to only 40 percent of those aged 65 and above. Similarly, understanding of tax brackets (Q17) was higher among younger respondents, with nearly 65 percent of those under 45 answering correctly, compared to 46 percent of those over 65.

These findings suggest that tax literacy may decline with age, potentially due to outdated knowledge or a lack of recent engagement with current tax information, highlighting the need for ongoing education efforts across all age groups and simplification of the tax code. There is a movement nationwide for financial literacy education, but this is a relatively new push for most states.

Interestingly, when it comes to perceptions about large tax refunds (Q19), older age groups (46 and above) are more likely to disagree with the idea that large tax refunds are beneficial, which suggests a better understanding of tax planning in these age groups. Specifically, 59 percent of respondents aged 46-65 disagreed with the statement, compared to only 38 percent of respondents aged 18-29.

Income and Tax Literacy

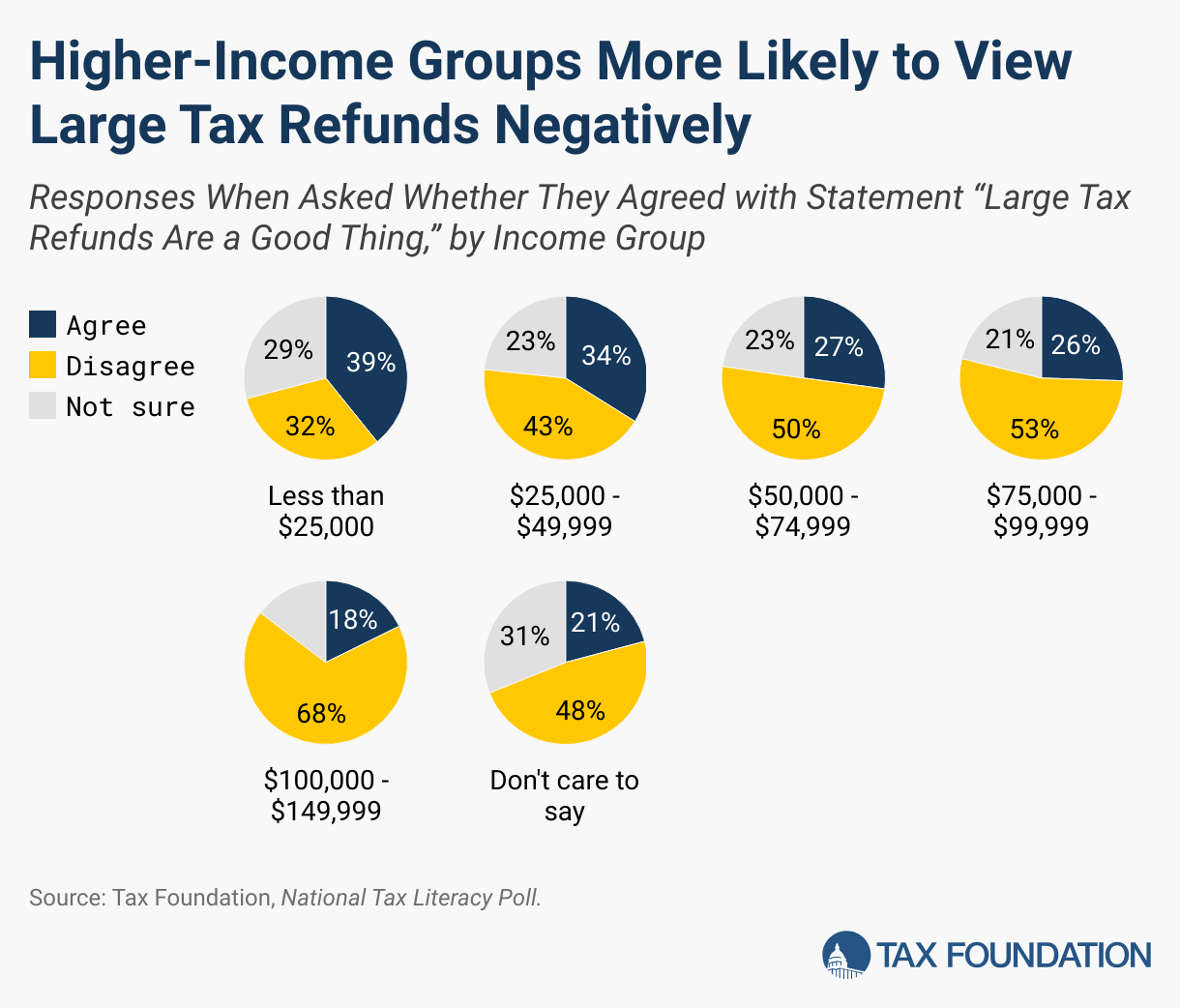

Income level is another significant factor influencing tax literacy. Generally, respondents with higher household incomes ($75,000 and above) tend to perform better on tax knowledge questions.

For instance, 66 percent of higher-earner respondents (earning between $100,000 and $149,999) correctly understood how progressive graduated-rate tax brackets work (Q17), compared to only 28 percent of those earning less than $25,000. This significant gap highlights a lack of awareness about higher tax brackets among lower-income groups, who are more likely to fall below the 22 percent tax bracket.

The analysis also showed that higher-income respondents are more likely to correctly identify other key tax concepts, such as the average federal income tax rate (Q15) and the tax burden of the top 1 percent of taxpayers (Q16). For example, 50 percent of respondents earning between $100,000 and $149,999 correctly identified the average tax rateThe average tax rate is the total tax paid divided by taxable income. While marginal tax rates show the amount of tax paid on the next dollar earned, average tax rates show the overall share of income paid in taxes.

, compared to just 32 percent of those earning less than $25,000.

When analyzing the perceptions of large tax refunds (Q19), it was found that over half of the respondents with incomes over $50,000 disagreed that large tax refunds are beneficial. In contrast, only one-third of lower-income respondents shared this view. This trend seems to highlight that those with lower incomes may feel more positive about receiving large refunds due to their immediate financial needs, prioritizing short-term benefits over long-term financial planning. As tax literacy plays a key role in financial literacy, these perceptions can impact sound financial planning for Americans.

Interrelationship Between Tax Knowledge Questions

A cross-analysis of the tax knowledge questions reveals that respondents who correctly answered more advanced questions, such as Q16 (the tax burden of the top 1 percent) or Q14 (the top federal income tax bracket), were also more likely to answer the basic questions, like Q17 (understanding how tax brackets work) correctly. For instance, 62 percent of respondents who answered Q16 correctly also got Q17 right, and 68 percent of those who correctly answered Q14 also correctly answered Q17.

Moreover, approximately 60 percent of those who demonstrated advanced tax knowledge disagreed that a large tax refundA tax refund is a reimbursement to taxpayers who have overpaid their taxes, often due to having employers withhold too much from paychecks. The U.S. Treasury estimates that nearly three-fourths of taxpayers are over-withheld, resulting in a tax refund for millions. Overpaying taxes can be viewed as an interest-free loan to the government. On the other hand, approximately one-fifth of taxpayers underwithhold; this can occur if a person works multiple jobs and does not appropriately adjust their W-4 to account for additional income, or if spousal income is not appropriately accounted for on W-4s.

is beneficial (Q19), indicating a correlation between tax literacy and alignment with certain tax policy perspectives.

Section B: Tax Perception Analysis

Main Takeaways

- Eighty-eight percent of respondents think the US federal tax code needs reform.

- Sixty-six percent of respondents think the US tax code is overly complex.

- Sixty-five percent of respondents think the US tax code is not fair.

- Sixty percent of respondents think the value of the federal government services they receive does not meet the value of what they pay in federal taxes.

- Fifty-nine percent of respondents think federal income taxes are too high.

- Only 11 percent of survey respondents think the federal budget deficit should be reduced by raising taxes, while 53 percent think it should be reduced by reducing spending.

Methodology/Background

For the tax perception section of our survey, respondents were asked thirteen questions about their perceptions of the US federal tax system. These questions ranged from whether the US tax code is fair, to whether businesses should pay more in taxes, to whether the value of government services received meets the perceived value of their federal tax payments.

The aim of this portion of the poll is to understand how American taxpayers feel about the federal tax system, identify patterns within demographics, and, when considered alongside the results of the tax literacy section, determine if tax literacy levels affect tax perceptions.

Analysis

Tax Reform

88 percent of respondents think the US tax code needs reform (Q12) with a clear consensus across political parties: 89 percent of Republicans, 88 percent of Independents, and 86 percent of Democrats believe so. However, there’s more debate about what exactly should be reformed (Q13): of those who call for tax reform, 42 percent think the distribution of the federal tax burden is the most important area to reform, 22 percent think the complexity of federal taxes is, 18 percent think the amount of tax collected is, 7 percent think the economic impact of federal taxes is, 1 percent think the neutrality of federal taxes is, 6 percent think something else is, and 3 percent are not sure.

It’s clear from these results that there is more than one pressing issue with the federal tax system in the minds of taxpayers. In the following sections, we explore each of these in more depth.

Income Taxes

Fifty-nine percent of respondents believe federal income tax rates are too high (Q1), including 83 percent of surveyed Republicans and 38 percent of surveyed Democrats. Twenty-seven percent of respondents believe federal income tax rates are just right, 6 percent believe they are too low, and 8 percent are not sure.

However, “too high” does not have a universally accepted definition (Q3). Thirty-one percent of respondents believe 10 percent would be a fair top tax rate on income, 20 percent believe 20 percent would be a fair top rate, 11 percent believe 30 percent would be a fair top rate, 8 percent believe 0 percent would be a fair top rate, 7 percent believe 40 percent would be a fair top rate, 10 percent would prefer a top rate higher than 40 percent, and 14 percent are not sure. For reference, the current top tax rate on income is 37 percent—higher than most respondents believe is “fair” (Q2).

Another discrepancy with this perception is that while most respondents want a lower top rate, 58 percent of respondents believe high earners should pay more. This belief holds across tax literacy levels. While this could be attributed to tax literacy, as few respondents know the current top tax rate, it is important to note that these discrepancies could also be due to respondents considering effective tax rates or tax loopholes in their belief.

Tax Distribution

Sixty-five percent of respondents believe the US tax code is not fair (Q2). Age and income seem to influence this belief: 79 percent of respondents aged 30-45 believe the US tax code is unfair, compared to 55 percent of those older than 65. Most respondents with a household income over $100,000 (70 percent) also think the tax code is unfair, compared to 57 percent of those with household income less than $25,000. Twenty-eight percent believe the US tax code is somewhat fair, only 3 percent think it is very fair, and 4 percent are not sure.

Fifty-eight percent of respondents believe the federal tax burden should change by having high earners pay more, with variation by political affiliation (Q9). Thirty-two percent of Republicans, 53 percent of Independents, and 85 percent of Democrats support increasing federal income tax rates on high earners. Interestingly, only 10 percent of respondents believe the distribution should change by having low earners pay less, while 9 percent would prefer to leave the distribution unchanged. For answers that contradict common proposals to redistribute the tax burden, 5 percent of survey respondents prefer having high earners pay less and 4 percent prefer having low earners pay more. Fourteen percent are unsure of their position.

Value of Government Services

Based on our findings, how much taxpayers value the government services they receive significantly impacts their views on tax distribution (Q11). Sixty-seven percent of respondents who believe the tax code is not fair say the value they receive from federal government services does not meet the value they pay in federal taxes.

Overall, 60 percent of respondents share this belief, including 73 percent of surveyed Republicans and 37 percent of surveyed Democrats. Twenty-five percent respond that the services they receive meet the value of their federal tax payments, 5 percent say services exceed the value of their federal taxes, and 10 percent are not sure.

Tax Complexity and Decision Making

Sixty-six percent of respondents believe the US tax code is overly complex (Q10), including 72 percent aged 30 to 45, 68 percent aged 46 to 65, 64 percent over 65, and 52 percent aged 18 to 29. Twenty-five percent think it is somewhat complex, 3 percent think it is not complex, and 14 percent are not sure.

Respondents who are categorized as “high earners” may believe the tax code is too complex because it becomes more complex for them, as they face additional taxes and provisions with more and varying types of income and assets.

While 42 percent of survey respondents admit to having made decisions about working, spending, donating, investing, or relocating based on tax impact, 46 percent report that taxes have never impacted their decision-making, and 12 percent are not sure (Q7). The influence of taxes increases with education level, with 31 percent of those with high school or less and 49 percent with a post-graduate degree reporting that they have made decisions based on their tax impact. The same trend is seen with income levels of respondents: 50 percent of those earning above $100,000 have made decisions based on tax impact, compared to only 31 percent of those making less than $50,000.

Business Taxes

While corporate taxes are legally paid by corporations, only 14 percent of respondents believe the corporation itself bears the cost or burden of these taxes, while 45 percent believe consumers bear the cost, 6 percent believe employees do, 5 percent believe shareholders do, 24 percent believe all parties do, and 5 percent are not sure (Q8). Most people are consumers, which could affect this perception. The results generally do not align with popular discourse regarding corporate tax burdens and higher taxes on businesses.

Respondents in favor of higher business taxes are less likely to believe that consumers bear the burden of corporate taxes. Among those who support higher business taxes, 40 percent believe consumers bear the burden of these taxes, while the majority, 54 percent, of those favoring lower business taxes share this belief.

Generally, American taxpayers are split about how much businesses should be taxed (Q5). Forty-one percent of all respondents think businesses should pay more in taxes, 23 percent think they pay the right amount, 21 percent think they should pay less in taxes, and 14 percent are not sure.

Child Tax CreditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly.

Preferences for the child tax credit are also mixed and highly dependent on the age of the respondent, most likely reflecting the number of children in the household and eligibility for the credit. Thirty-nine percent of respondents think the child tax credit should be increased, 36 percent believe it should be kept as is, 14 percent think it should be decreased, and 10 percent are not sure. Fifty-four percent of respondents aged 30 to 45 think it should be increased, compared to 33 percent of those older than 65 (Q6).

Interestingly, of those with a household income greater than $100,000, 46 percent believe the child tax credit should be increased, and 11 percent believe it should be decreased, but of those with a household income less than $25,000, 36 percent believe it should be increased, and 22 percent believe it should be decreased. This, too, likely reflects the number of children people have and eligibility for the credit, as higher-income households tend to have more children.

Deficit Reduction

Only 11 percent of survey respondents think the federal budget deficit should be reduced by raising taxes, while 53 percent think it should be reduced by reducing spending, 30 percent think it should be reduced by a combination of the two, and 6 percent are not sure (Q4). Support for reducing spending is consistent across income levels and educational attainment.

Respondents are polarized on this issue. Eighty-three percent of surveyed Republicans, 56 percent of Independents, and only 25 percent of surveyed Democrats believe the deficit should be reduced by spending cuts; 2 percent of surveyed Republicans, 9 percent of Independents, and 22 percent of surveyed Democrats believe the deficit should be reduced by raising taxes.

This was included in the survey as a current political issue for taxpayers considering the fiscal health of the US and the looming federal deficit.

Section C: How Tax Literacy Affects Tax Perception

Main Takeaways

- Fifty-nine percent of those “proficient” in tax literacy believe consumers bear the burden of corporate taxes, compared to 44 percent of “beginners” and 46 percent of “intermediates.”

- Only 33 percent of those who believe that the federal tax distribution should change by having high earners pay more know the correct top income tax rate.

- Of those who believe that the tax code is not fair, only 35 percent know the correct top income tax rate.

- Only 18 percent of those who believe that the federal tax distribution should change by having high earners pay more know the correct percentage of federal income taxes paid by the top 1 percent. Fifty-eight percent of all respondents support this.

- Of those who believe that the tax code is not fair, only 21 percent know the correct percentage of federal income taxes paid by the top 1 percent.

- Of those who believe that the most important tax code reform is readjusting the distribution of the federal tax burden, only 20 percent know the correct percentage of federal income taxes paid by the top 1 percent.

Analysis

Tax literacy significantly influences individuals’ perceptions of the tax system, with those possessing higher levels of tax knowledge generally having a more realistic understanding of tax policies and their effects. However, the widespread lack of accurate tax information among those who desire changes to the tax code highlights the need for enhanced tax education as well as more simplification of the tax code. This could play a crucial role in enabling more informed public debate on tax policy and fostering more informed opinions on the fairness and structure of the US tax system.

Who Bears the Burden of the Corporate Income TaxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

?

The economic evidence suggests that in the long run, workers and consumers, rather than shareholders, bear a sizable share of the corporate tax burden.

A higher level of tax literacy appears to correlate with a more accurate understanding of how corporate taxes are ultimately passed on to consumers. Among respondents with a proficient level of tax literacy, 59 percent believe that consumers bear the burden of corporate taxes. In contrast, only 44 percent of beginner-level respondents and 46 percent of intermediate-level respondents share this belief.

Do Advocates for Changes in Federal Tax Distribution Understand the Top Income Tax Rate?

The analysis reveals a gap in knowledge regarding the top income tax rate among those advocating for changes in the federal tax distribution.

Many respondents who are critical of the current tax structure may lack accurate information about existing tax rates, potentially skewing their views on how the tax system should be reformed. For instance, only 33 percent of respondents who believe that high earners should pay more in taxes correctly identified the top income tax rate, compared to 58 percent of the overall sample. Similarly, just 35 percent of those who view the tax code as unfair knew the correct top income tax rate.

Understanding of Federal Income Taxes Paid by the Top 1 Percent

A large portion of those advocating for increased taxation on high earners may not be fully informed about the current distribution of the tax burden, leading to potential misconceptions about the equity of the tax system.

Among respondents who believe that the federal tax distribution should be adjusted so that high earners pay more, only 18 percent know the correct percentage of federal income taxes paid by the top 1 percent of earners. This knowledge gap is also pronounced among those who perceive the tax code as unfair, with only 21 percent correctly identifying the share of taxes paid by the top 1 percent.

Additionally, just 20 percent of respondents who prioritized adjusting the distribution of the federal tax burden as the most important reform know the correct percentage of taxes paid by the top 1 percent.

Conclusion

Most American taxpayers do not understand and are dissatisfied with the tax code. These findings generally hold true across income levels, educational attainment, political affiliation, and age.

In 2023, Americans filed 271.5 million tax returns. Of these, nearly 71 percent, or 192.3 million, were individual and corporate income tax returns. According to the latest estimates from the White House Office of Information and Regulatory Affairs (OIRA), Americans will spend more than 7.9 billion hours complying with IRS tax filing and reporting requirements in 2024. This burden and the clear misunderstanding of the tax code point to a need for simplification.

The significance of this is large, as most US adults are taxpayers. The tax code plays a role in our daily lives through earnings, budgets, savings, investments, location, and more. Misunderstanding the tax code not only influences how we perceive it, but it can also change our lives in significant ways, such as affecting how we approach financial planning.

With only about 2 percent of respondents being “proficient” in tax literacy, there is significant work to be done in tax education across the country.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Appendix

Survey Questions

Q1 Do you think your federal income tax rates are too high, too low, or just right?

Q2 Do you believe the U.S. tax code is very fair, somewhat fair, or not fair?

Q3 What do you think would be a fair top tax rate on income: 0%, 10%, 20%, 30%, 40%, or higher?

Q4 Do you think the national deficit should be reduced by raising taxes, reducing spending, or both?

Q5 Do you think businesses should pay more in taxes, less in taxes, or do you think businesses are taxed about the right amount?

Q6 Do you think the child tax credit should be increased, decreased, or kept as-is?

Q7 Have you ever made any of the following decisions based partially on their tax impact: worked less to avoid being taxed in a higher bracket, relocated or moved where you live, purchased or not purchased a product or service, made an investment or saving decision, or donated to charity?

Q8 While corporate taxes are legally paid by corporations, who do you think bears the cost of these taxes: the corporation itself, shareholders, employees, or consumers?

Q9 From the following list of choices, how do you think the distribution of the federal tax burden should change: by having high earners pay more, by having high earners pay less, by having low earners pay more, by having low earners pay less, or do you think the distribution is about right and we shouldn’t change it?

Q10 Do you believe the U.S. tax code is overly complex, somewhat complex, or not complex?

Q11 How do you feel about the value you receive from federal government services – would you say that value meets, does not meet, or exceeds the value of what you pay in federal taxes?

Q12 Do you think the U.S. federal tax code is in need of reform, or not?

Q13 From the following list of choices, which aspect of the federal tax code do you think is in most need of reform: the amount of tax collected, distribution of the federal tax burden, economic impact of federal taxes, complexity of federal taxes, neutrality of federal taxes, or something else?

Q14 I’m going to ask you some questions about taxes and ask you to answer to the best of your knowledge. Here’s the first one: to the best of your knowledge, what tax rate applies to the top U.S. federal income tax bracket: 22%, 32%, 37 % or 43%?

Q15 To the best of your knowledge, do you think the average U.S. federal income tax rate is 3-4%, 13-14%, or 25-26%?

Q16 To the best of your knowledge, how much do you think the top 1% of taxpayers by income account for in terms of share of total federal income taxes paid: 1%, 12%, 42%, or 64%?

Q17 Suppose your income places you in the 22% bracket—how much of your income do you think is taxed at a rate of 22%: just some of it, or all of it?

Q18 Suppose you are being taxed at a rate of 10% on $10,000 of income, which do you think is more valuable to you: a $1,000 income tax deductionA tax deduction is a provision that reduces taxable income. A standard deduction is a single deduction at a fixed amount. Itemized deductions are popular among higher-income taxpayers who often have significant deductible expenses, such as state and local taxes paid, mortgage interest, and charitable contributions.

or a $1,000 income tax credit, or do you think those are the same thing?

Q19 Do you agree or disagree with the following statement: Large tax refunds are a good thing.

Share this article