Products You May Like

Key Findings

- Legal sports betting in the U.S. hit an all-time high in 2023 at more than $100 billion wagered.

- States collected more than $1.8 billion in taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

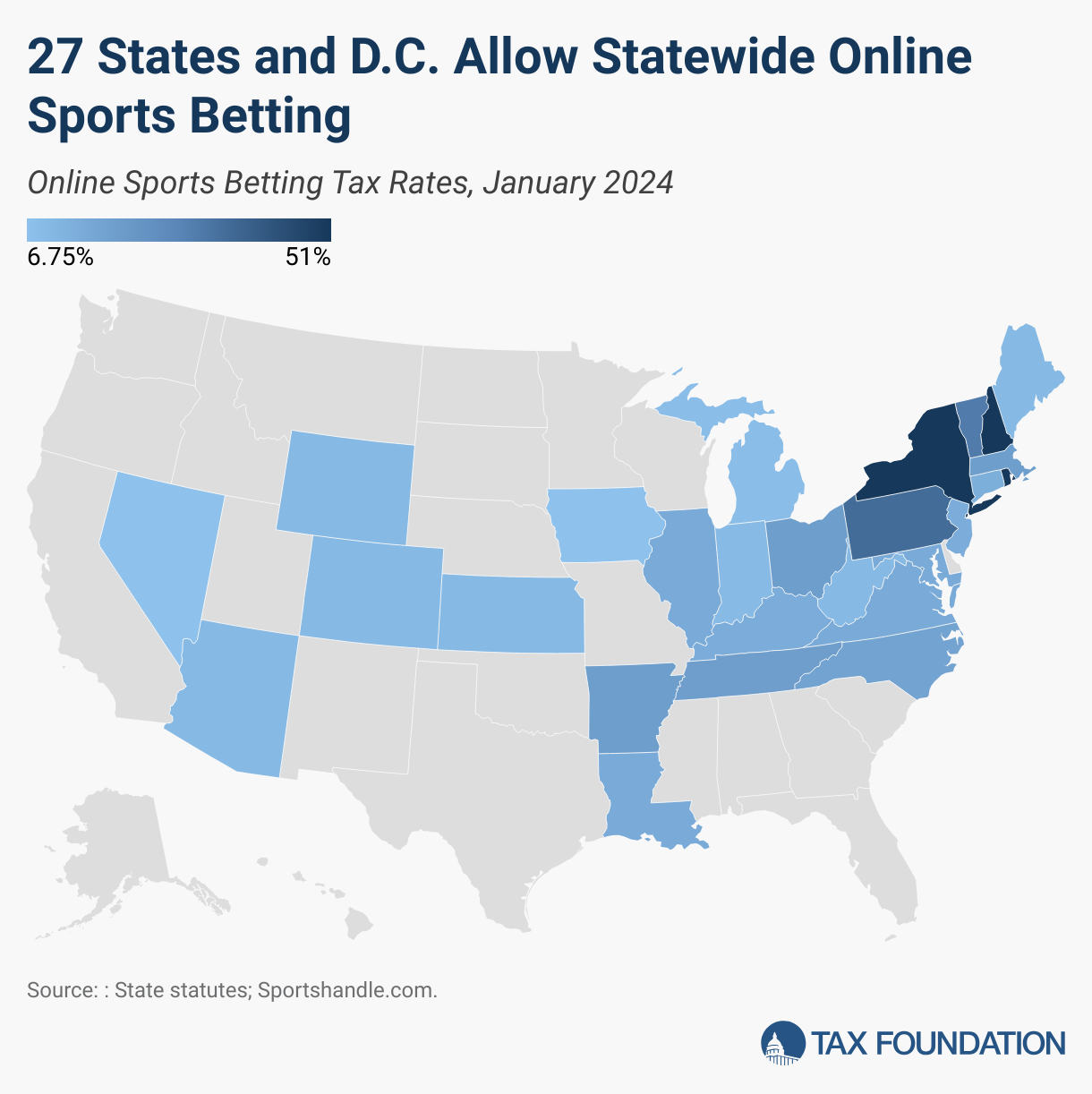

revenue from sports betting taxes in fiscal year 2023. - State statutory sports betting tax rates range from 6.75 percent in Nevada and Iowa to 51 percent in New Hampshire, New York, and Rhode Island.

- New York generated more than $800 million in sports betting tax revenue in 2023, while South Dakota raised less than $100,000.

- Low-rate taxes based on net gaming revenue make an effective tax design.

Introduction

Consumers legally wagered more than $100 billion on sporting contests in 2023, creating more than $1.8 billion in state revenue. Sports betting is now legal in 38 states and the District of Columbia, and the landscape is rapidly evolving.

The sports gaming industry has been transformed over the past six years. On May 18, 2018, the Supreme Court struck down the anti-sports-betting Professional and Amateur Sports Protection Act in Murphy vs. NCAA, granting states the ability to regulate sports betting independently. Many states quickly responded by establishing their own marketplaces. Each year since 2018 has seen an increase in the number of states with legal sports betting markets.

Beyond the court decision, tax policy was the key to the development of legal sports betting markets. Tax revenue was the carrot many state policymakers needed to support legalizing sports betting. Policymakers could apply a targeted tax on sports wagers or net gaming revenue to help raise revenue and mitigate problems that could come with larger betting markets.

Targeted taxes on sports wagering rely on the economic justification that gambling is addictive. Therefore, public funds can be used to improve the well-being of those who need help breaking their addiction. Sports betting taxes can be used to raise revenue to support those addicted players. Some state taxes—and the expenditures they support—hew better to this justification than others.

A sports wagering tax should be simple and transparent, cost little to administer, give equal treatment to comparable wagering activities, and produce stable revenue. Broadly summarized, sports betting taxes should carry a low rate and apply to the broad sports wagering tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.

. The federal government and the states have designed a variety of ways to tax sports betting, some more effective than others. The lessons learned from these early taxing strategies can help inform effective policy for future reform and adoption of sports betting taxes in new states.

Sports Betting

The sports betting world is loaded with technical jargon. Before we examine tax structures on sports betting, it may be helpful to define the terms commonly associated with business operations and tax in sports betting.

Line: The terms of a wager.

Handle: The total dollar amount wagered. The handle can be subdivided into the cash handle, representing all bets made with cash, and promotional wagers, which are combined to make the total handle.

Gross Gaming Revenue (GGR): The total dollar amount wagered minus the amount that is returned to players (RTP) for their winning bets.

GGR = Handle – RTP

Hold Percentage or Gross Gaming Revenue Margin (GGRM): The sportsbook’s winning percentage of the total amount gambled.

Hold = GGR / Handle

Net Gaming Revenue (NGR): The sportsbook’s gross gaming revenue, subtracting out promotional wagers, free bets, and player incentives.

NGR = GGR – Promotional Wagers

Consider a line that reads

Team A -1.5 (-110)

Team B + 1.5 (-110)

This line tells bettors that Team A is favored by 1.5 points. Team A would need to win by 2 or more points for bettors placing their wager on Team A to win the bet.

The (-110) tells bettors that they need to place a wager of $110 to win $100. A winning bettor will walk away with $210—the original $110 wagered plus the $100 win. Losing bettors get $0. The

(-110) also advertises the sports betting operator’s odds advantage, 4.5 percent in this example.

Table 1 illustrates a few hypothetical wagers and presents the revenue, hold, and tax calculations. We assume a simple scenario with $1,100 wagered on each team. Regardless of the outcome of the game—Team A wins or Team B wins—the sportsbook collects $2,200 in wagers and returns $2,100 to winning bettors, earning GGR of $100 or a 4.5 percent hold.

Table 1. Gaming and Tax Revenues Can be Affected by Tax Design

Hypothetical Wagers, Revenues, and Tax Calculations

Hypothetical Wagers, Revenues, and Tax Calculations

Source: Author’s Calculations

Tax Design

While sports betting can be complex, sports betting taxes need not be. A simple tax on net gaming revenue scales with the profitability of gaming for sportsbooks. An excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections.

on the cash-only handle would be an appropriate tax base for an excise tax and could achieve similar goals to a low-rate NGR tax, but handle taxes risk becoming overly punitive, as the taxes rapidly increase as a percentage of NGR as tax rates or promotional wagers increase. Any tax on the handle or GGR includes taxing “phantom” wagers from promotional bets.

Table 1 illustrates tax collections from the hypothetical wagers described above. In the case of no promotional wagers, tax collections from a 10 percent NGR tax generates $10, while a 5.5 percent GGR tax and a 0.25 percent handle tax produce $5.50. The NGR tax collections amount to 10 percent of NGR, while the GGR and handle tax would be 5.5 percent of NGR.

Suppose that $45 of the handle actually came from promotional wagers, however. Column 2 illustrates how the tax collections change when accounting for promotional wagers. The sportsbook collected no money from bettors for these wagers, but paid out bettors’ winning picks. Deducting the $45 in promotional wagers decreases NGR to $55 for the sportsbook.

A tax based on NGR brings in less revenue in this scenario. The 10 percent NGR tax, 5.5 percent GGR tax, and 0.25 percent handle tax would all generate $5.50. While the NGR tax remains 10 percent of NGR, the GGR and handle tax now also comprise 10 percent of NGR, highlighting that taxes based on GGR or the handle increase as a percent of GGR as promotional wagers grow.

For comparison, effective tax rates on major American industries average 19.3 percent. Transportation and warehousing face a relatively low effective tax rate of 10.3 percent, while manufacturing faces a relatively high effective tax rate of 23.8 percent.[1] Exorbitant tax rates set by certain states threaten to make sports betting an outlier among American industries, facing an excessively large tax burden.

Promotional Wagers and Free Bets

Tax treatment of promotional wagers and free bets is one of the biggest issues surrounding sports wagering taxes. To push tax collections higher, most states now impose sports betting taxes on operators’ GGR. The result is an interesting case of over-taxation, in which sportsbooks effectively pay taxes on bets for which they received no revenue.

Promotional wagers are a common tool sportsbooks use to attract new customers or attempt to gain market share. A wide variety of sportsbook promotions exist, but we’ll use an example of a simple promotion for illustrative purposes.[2]

Suppose a sportsbook offers a deposit match of $110 in site credit for signing up for the platform. After you sign up, and deposit $110, you can use your matching “free” $110 to make any bet you like on the site after you place a bet with the other $110 you deposited.

You decide to place two wagers on two separate sports games, each with a line of -110. You place your $110 cash wager on the first game and you use your promotional deposit match of $110 to wager on a second game. You have a lucky streak and win both wagers! Your $220 in initial wagers is returned to your account along with your $200 in winnings, bringing your total account balance up to $420. You decide to cash out your winnings.

The tax question here is how to treat the $0 “free deposit match” that you wagered and turned into a $200 cash payment. Standard business accounting would have the sportsbook add no money to their top-line revenues—no money was wagered—and then account for the $200 as an expense. Net betting proceeds should decrease by $200, along with any other measure of the sportsbook’s profitability.

If tax collections are based on NGR, then tax collections and NGR both decrease as sportsbooks offer more promotional wagers. However, offering more aggressive promotional wagers to reduce sports betting tax liabilities is not a viable strategy, financially speaking. An operator that pursues more aggressive promotional strategies can effectively reduce its tax liability in the short-term, but promotional wagers have a disproportionately larger impact on bottom-line profitability than tax liability.

Nevertheless, because tax collections decrease as promotional wagers increase, this can give the perception that sportsbooks are being undertaxed because tax collections as a percentage of GGR, less deductions from free bets, will be lower than the implied state GGR tax rate.

Colorado provides a good example. Colorado established a 10 percent tax rate on net betting proceeds in 2021. In 2022, statewide sportsbook GGR was $351 million. After reducing statewide GGR by promotions, free bets, and other permissible deductions, Colorado collected $19.7 million in tax revenue. Tax collections made up 5.6 percent of pre-deduction GGR, substantially less than the rate of 10 percent that some policymakers expected. This is the correct outcome, but the reaction was representative of the understandable confusion about these taxes and how to appropriately measure profits.

Even with an accurate forecast of the handle’s size, failing to account for the effects of promotional bets and other deductions can lead to a substantially inaccurate estimate of tax revenue. Starting January 1, 2023, Colorado limited a sportsbook operator’s monthly untaxed free play offerings to no more than 2.5 percent of the handle. This will result in a smaller gap between GGR and NGR, but that does not imply higher tax revenues, because tax collections are based on the amount of net revenues, not their relative share. There will be fewer deductions, but only because there are fewer promotional bets. If a reduction in promotional bets has no impact on the number of paid bets—if, in other words, the bets weren’t the sort of inducement the sportsbooks expected—then the state’s revenue will remain constant, even though the GGR declines. If a reduction in promotional play results in fewer paid bets as well (that is, the promotions were working), then revenue would decline relative to the previous policy, even though the effective rate on GGR will be higher.

Access to Sports Betting Markets

Another issue at the forefront of sports gaming tax policy is access to legal sports betting markets. Most states have legalized some form of online sports betting. Among states that have legalized online sports betting, some of those states limit access to their legal markets. This is done primarily by creating high barriers to sports betting operators who wish to offer services in the state and by limiting the geographic locations at which players are allowed to place bets.

States enjoy wide latitude in how they establish betting activities, and consequently, have created a spectrum of barriers to market entry for sports operators. Common barriers facing operators include expensive licensing fees and requirements for online sportsbooks to partner with existing in-state, brick-and-mortar operators.

While Nevada, South Dakota, and Mississippi charge licensing fees that are $5,000 or less, sportsbooks operating in Massachusetts must pay an initial fee of $5 million with another $5 million renewal fee every five years. Sportsbooks in Pennsylvania are required to pay a one-time fee of $10 million and a $250,000 renewal fee every five years.

The licensing fee in New Jersey is “only” $100,000. However, New Jersey requires that online sportsbook operators partner with a licensed brick-and-mortar racetrack or casino in the state. Ohio offers online sportsbooks the option to partner with a professional sports organization approved by the Casino Control Commission (e.g., the Columbus Blue Jackets, the Cleveland Cavaliers, or the Cincinnati Reds) to offer mobile sports wagering.

Other states mandate a partnership with the state lottery commission or hand control of online sports betting markets to the state lottery commission. In Connecticut, “master wagering licensees”—those permitted to offer online sports betting—include the Mohegan Tribe, the Mashantucket Pequot Tribe, and the Connecticut Lottery. Online gaming operators wishing to offer services in Connecticut must partner with one of those groups.

This differs from Montana, which monopolized all sports betting. The Montana Lottery Commission has full operational control of online sports betting, so market-leading sportsbooks like DraftKings and FanDuel are unavailable in the state.

Several states also restrict where players can gamble online. In Delaware, Mississippi, Montana, New Mexico, North Dakota, South Dakota, Washington, and Wisconsin, would-be gamblers can only place bets at select locations such as retail casinos, state-operated facilities, or on tribal lands. These bettors may or may not have access to online betting platforms at each facility.

These practices substantially hinder consumers from participating in legal markets and generate less tax revenue. Frequently, moreover, the hindrances appear arbitrary or more focused on economic or political preferences, not consumer harms: their designs often seem to have less to do with limiting problem gaming than they do with increasing state control or favoring particular operators. Sports betting markets should be easy to access with simple taxes. Despite numerous examples of well-functioning markets, access to markets and tax rates vary across the country.

Further Considerations for Tax Design

The outcomes of state experiments in sports gaming tax design over the rapid post-Murphy expansion offer several other key lessons. Notably, administering tax policy through state gaming commissions instead of state departments of revenue creates challenges; tax rate stacking across multiple layers of government is important to consider; and tax designs that are prohibitively high or restrictive to players are suboptimal.

States with legalized sports wagering markets typically assign regulatory and taxing authority to the state’s gaming commission, making it responsible for tasks that are typically performed by state departments of revenue (DOR). In some cases, this results in administrative challenges for sportsbooks that are forced to comply with the unique treatment of tax issues arising from the decisions of an agency less accustomed to administering taxes. Sometimes, gaming regulators require gaming operators to adopt specific accounting practices that constrain sportsbooks’ accounting choices, whereas other businesses would enjoy a wider range of accounting options based on state statutes. Gaming regulators also sometimes dictate business decisions that affect tax liability. All businesses, of course, must comply with the obligations of the tax code and use appropriate accounting standards, but businesses also face an array of options about how to conduct their business, some of which have different tax implications. Within the bounds of the law, they may arrange their affairs to limit tax exposure rather than make economic choices that would magnify their liability. Within sports betting, however, businesses can find their choices dictated by state agencies in ways that maximize their tax exposure.

Sportsbook taxes, receipts, and regulatory practices are often audited daily, and gaming regulators require all tax returns to reconcile to the penny with the daily regulatory reporting. If corrections are needed, sportsbook operators are often not permitted to make manual adjustments to tax returns without prior written approval from the gaming regulators even when such manual adjustments are necessary to ensure the amounts reported on the returns comply with the respective gaming regulators’ own tax positions.

This makes long-run tax planning difficult or impossible for sportsbooks to implement effectively. Operating a tax system through the state gaming commission puts many operators in a disadvantageous position compared to other businesses operating within a state and across multiple states.

Unlike state DORs, gaming commissions rarely have a formally established process for amending prior tax returns or claiming tax refunds, for example. North Carolina’s recently launched sports betting industry, however, is being administered by the North Carolina DOR. The North Carolina DOR launched an online sports betting tax filing portal and issued accompanying formal tax return instructions before sports betting commenced in the state. In addition, the North Carolina DOR published formal sports betting tax FAQs that they then continually updated to address additional comments received from sports betting operators.

Other regulations or mandates can also substantially hinder legal sports betting markets. Tennessee, for example, initially mandated that sportsbooks hit at least a 10 percent hold each month. Beyond the fact that this hold rate exceeds the national average, mandating a winning percentage on operators offering wagers on games of chance proved folly. In 2022, 9 of the 11 registered sportsbooks in Tennessee failed to meet the 10 percent hold requirement and were subject to a $25,000 fine.[3] Tennessee has since repealed the minimum hold mandate and now applies a 1.85 percent tax on the handle.

Tax policy should also align across federal, state, and/or municipal governments. The calculations in Table 1 illustrate that the federal excise handle tax can generate at least as much revenue as state taxes on GGR or NGR. Operators must pay that federal tax in addition to state taxes. Wherever there are multiple layers of taxation, consistency in approach simplifies tax policy.

Prohibitively high tax rates and overly restrictive betting restrictions incentivize bettors to head to illicit (untaxed) markets. These suboptimal policies can overly burden sportsbooks and under-deliver products demanded by consumers. The results are fewer gains from trade in legal markets and possibly much less tax revenue.

Current Tax Rates

Most states have agreed to legalize sports wagering. However, large disparities persist in the design and tax treatment of sports betting activities.

In most states that have legalized sports betting operations, consumers have access to gambling operations statewide. They can gamble online or in person, and the tax rates for such activities are the same regardless of how or where they gamble.

In other states, online wagers are treated differently from wagers placed in person. In Kentucky, Louisiana, Massachusetts, New Jersey, and New York, online wagers are taxed more heavily than retail (in-person) wagers. Table 2 illustrates the range of tax rates applied to online and retail wagers.

Table 2. States Apply a Wide Range of Tax Rates to Sports Gaming Revenues

Online and Retail Tax Rates, January 2024

Notes: Notes: The Montana Lottery Commission operates all state sports betting operations. Tennessee applies a 1.85% handle tax; we conver this to a GGR equivalent rate using the national average of a 9.4 percent handle. The District of Columbia currently operates unders a revenue sharing agreement for online operators in lieu of a percentage excise tax. Vermont also engages in a revenue share agreement; as of February 2024, the average revenue share was 31.7 percent. The New Jersey adds a 1.25 percent Economic Development Tax to all online and retail sports wagers in addition to its statutory rate. Localities in Pennsylvania (2% statewide included in rates stated above), Illinois (Cook County applies a 2% tax, not included in the rate above), and Michigan (Detroit applies a 1.25% tax, not included above).

Sources: State Statutes; Bloomberg Tax

Effective tax rates often vary substantially from statutory rates, making apples-to-apples comparisons across states based on statutory rates misleading. This results primarily from states’ treatment of promotional wagers and the selection of the tax base.

A sports betting operator’s effective tax rate on NGR will always be higher than the statutory rate in states with GGR tax regimes, unless the operator accepts no promotional wagers (which we have no record of that occurring). Further, a sports betting operator’s effective tax rate on NGR continues to increase as the percentage of handle received as promotional wagers increases. Because New York prohibits sportsbooks from deducting any promotional wagers from GGR, for example, the only way for a sports betting operator to achieve a 51 percent effective wagering tax rate on NGR in New York is to accept no promotional wagers. By accepting any promotional wagers, an operator’s effective wagering tax rate on NGR will be greater than 51 percent with that effective wagering tax rate on NGR.

We simulate how effective tax rates vary based on whether states’ tax base allow sports operators to deduct promotional wagers from GGR. The final column of Table 2 shows tax collections as a percentage of NGR for a simulated 8 percent hold and promotional bets that comprise 3 percent of the total handle.

Tax collections as a percentage of NGR increase to a staggering 81.6 percent for New Hampshire, New York, and Rhode Island. Because Michigan allows promotional deductions, the state has the lowest effective tax rate for sportsbooks, at 8.4 percent.

While 38 states have legalized sports wagering in some capacity, bettors only have statewide access to online sports betting platforms in 27 states and the District of Columbia due to restrictions in some states on where wagers can be placed (e.g., at casinos or on tribal lands). Nevada and Iowa apply the lowest tax rates at 6.75 percent. Figure 1 shows the distribution of online sports betting tax rates across U.S. states.

New Hampshire, New York, and Rhode Island apply the highest tax rate to sportsbooks at 51 percent. However, these statutory rates don’t tell the entire story. New Hampshire and Rhode Island are single-operator states, in which one company (DraftKings in New Hampshire and International Gaming Technology in Rhode Island) contract with the state to run a monopoly sports wagering market. New York has a competitive market with multiple companies offering sports betting services.

Tax Revenues

Sports gaming revenues have served as a windfall revenue source for states. In the last month of fiscal year 2018, only three states permitted commercial sports wagering, collecting just $2.1 million in June 2018. By June 2023, 30 states had operational sports wagering markets, generating more than $119 million in monthly tax revenue.

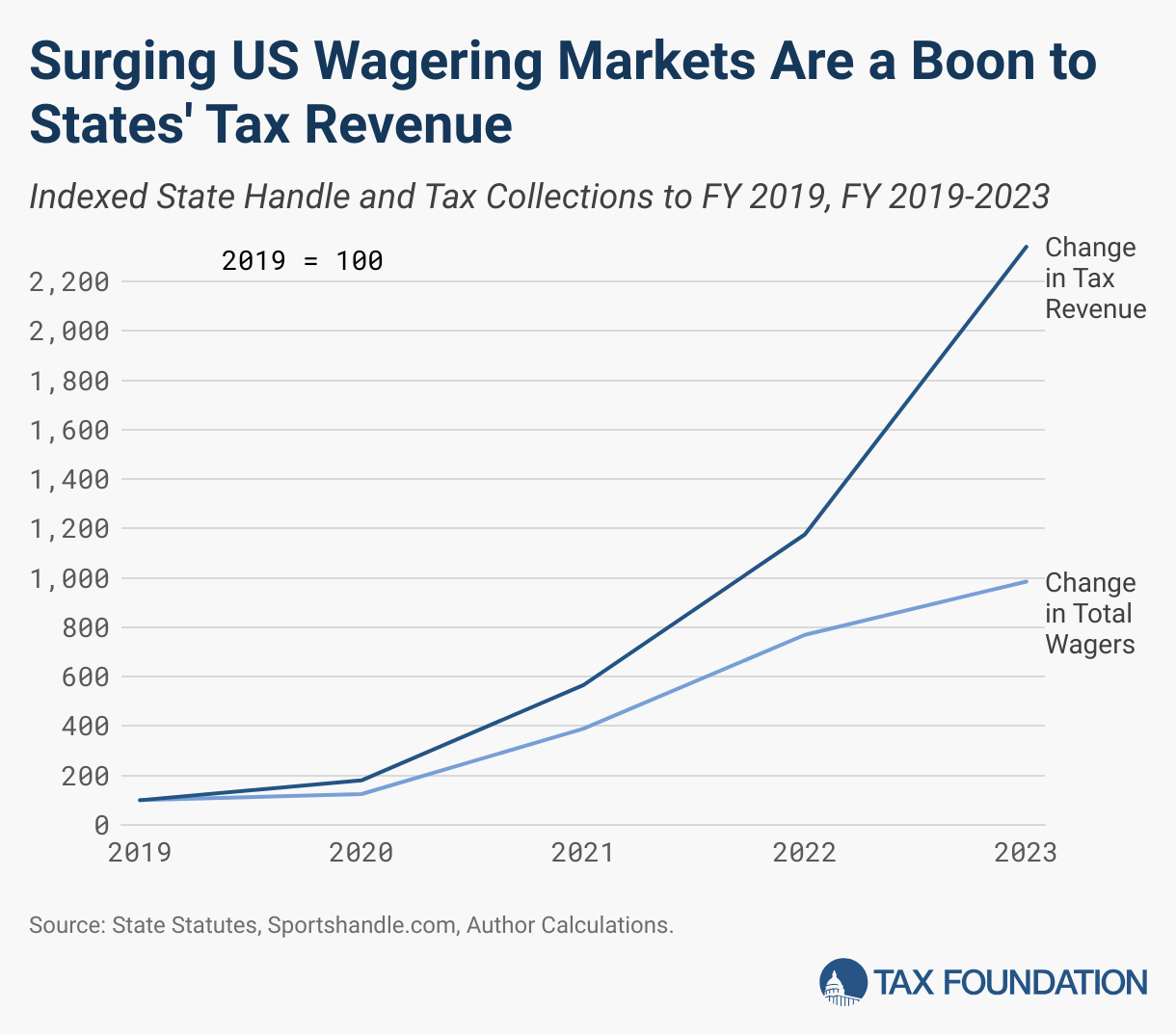

The rapid expansion of legal sports wagering is illustrated in Figure 2 below. With more states facilitating legal sports wagering, total U.S. wagers (handle) grew nearly tenfold from 2019 to 2023, from $10.4 billion to $102.8 billion. State tax revenues for the same period grew more than twentyfold, from $79 million to more than $1.85 billion.

Table 3. Surging US Wagering Markets Create Nearly $2 Billion in Tax Revenues for States

State Handle and Tax Collections, FY 2019-2023

Sources: State Statutes, Sportshandle.com, Author Calculations.

The expansion of sports betting into new states has been the biggest driver of the growth of legal wagers and tax revenues. New York adopted statewide legal sports betting markets in January 2022. In fiscal year 2023, New York raised more than $800 million in tax revenue from sports betting, 43.2 percent of nationwide sports betting state tax collections.

Table 3 shows the handle, GGR, hold, and tax collections from all states that reported legal sports gaming revenues in fiscal year 2023.

Table 4. State Tax Collections from Sports Wagering Approach $2 Billion

State Wagering Handle, Gross Gaming Revenue, Hold, and Tax Collections in Fiscal Year 2023

Notes: * Figures from Ohio and Kansas represent only a partial fiscal year of operations

Sources: State Statutes, Legalsportsreport.com, and author calculations.

After New York’s $800 million in revenue, Pennsylvania, Illinois, and New Jersey each brought in more than $100 million. South Dakota, Wyoming, and Montana brought in the least revenue, each less than $1.5 million. South Dakota and Montana both limit the locations at which bettors can wager online. Wyoming has no retail sportsbooks; all sports gaming revenue is generated online.

Nationwide, the average hold was 9.4 percent. This is more than double the hold in our perfectly balanced sports wager example in Table 1. This shouldn’t be too surprising, though, as gamblers don’t always prefer bets with the best odds. Casino attendees don’t only play perfect games of blackjack or bet on red/black on roulette (games that traditionally offer some of the best odds for players).

This also means that sportsbooks return to players more than $9 for every $10 wagered. That return trumps every state lottery in the county, by a lot. State lotteries return about 60-65 percent to players on average.[4]

With states like Texas and California not yet operating legal sports wagering markets, nationwide adoption of legal sports wagering has the potential to more than double the size of the current market. Tax revenues will continue to grow with the expanding market.

As the tax base grows, tax policy design becomes increasingly important. Rates should be low enough to pull participants out of black markets and into the legal, regulated markets, and stable enough not to rely on bettors doing particularly poorly for the state to generate revenue.

A low-rate tax on net gaming revenue with relatively low compliance costs can accomplish all these tax goals.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

[1] Cody Kallan and Garret Watson, “Who Gets Hit by the InflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.

Reduction Act Book Minimum Tax?,” Tax Foundation, Aug. 11, 2022, https://taxfoundation.org/blog/book-minimum-tax-analysis/.

[2] Tyler Maher, “Best Sportsbook Promotions – Sports Betting Promos Explained,” Forbes, Jan. 24, 2024, https://www.forbes.com/betting/sports-betting/best-sportsbook-promotions/.

[3] Tennessee General Assembly Fiscal Review Committee, “Fiscal Memorandum SB 475 – HB 1362,” Apr. 18, 2023, https://www.capitol.tn.gov/Bills/113/Fiscal/FM1360.pdf.

[4] Amelia Josephson, “The Economics of the Lottery in the U.S.,” SmartAsset, Aug. 25, 2023, https://smartasset.com/taxes/the-economics-of-the-lottery.

Share this article