Products You May Like

The US vaping market is a disaster. As much as 98 percent of vaping products sold in the US are illicit. Most states levy an excise tax on vaping products, but these taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

systems vary substantially. The result is a messy tax system covering largely illicit products, and no one knows whether taxes are being collected and remitted on most products sold nationwide.

How Did the Vaping Market Become Such a Mess?

Unlike the standard process for selling products in a market economy—where entrepreneurs and innovators can immediately sell their products to consumers—nicotine or tobacco companies must receive written permission (a marketing order) from the Food and Drug Administration (FDA) to legally market a new nicotine or tobacco product in the United States. Any tobacco or nicotine product lacking a marketing authorization order from the FDA cannot legally be sold in the United States.

The FDA has been extraordinarily slow and stringent when it comes to authorizing products for sale. From October 2019 to March 2024, the FDA received approximately 26.6 million premarket tobacco product applications (PMTAs). Of those 26.6 million applications, the FDA agreed to review roughly 1.2 million (rejecting the rest). Of the 1.2 million files reviewed, the FDA granted marketing granted orders (MGOs) for 30 products—just 0.001 percent of new product applications.

It took the FDA until June 2024 to issue the first MGO for a flavored product—four versions of NJOY Menthol. The vaping market, however, has demonstrated strong demand for a variety of flavors, not just menthol. Without legally authorized products available for sale, illicit products quickly filled the void to meet consumer demand.

Illicit vapes were perfectly situated to take over the vaping market. They provided sizable markups for retailers and may have also had a pricing advantage over legal vapes, as some retailers didn’t charge and remit taxes on products that weren’t legally available for sale. And there continues to be exceptionally weak enforcement of product prohibitions.

The primary tool in the FDA enforcement arsenal is a warning letter. As of June 2024, the FDA has issued more than 1,100 warning letters to manufacturers, importers, distributors, and retailers. In February 2023, the FDA filed the agency’s first civil money penalty complaints against four e-cigarette manufacturers.

In May 2023, the FDA attempted to block Chinese imports of market leader, Elf Bar, by ordering customs officials to seize incoming shipments. Elf Bar products didn’t have an FDA MGO, but their products were available nationwide, including flavors like strawberry melon and bubble gum. In response, Elf Bar changed its product names (e.g., EBCreate) to those not on the seizure list and products continued to flow from China into the US.

Are Illicit Vaping Products Taxed?

Determining whether illicit products are being appropriately taxed is a difficult endeavor. Data on illicit markets and products are scarce. Vaping tax data is also not granularly reported across taxing jurisdictions. In an attempt to answer this question, we instead use the variation in US state vaping tax rates, combined with data on market prices, to look for irregularities. Our data illustrate that the pricing of small-market and Chinese vaping products—those without an MGO—does not mimic pricing patterns we observe in products granted an MGO for which we know taxes are being applied.

Unlike cigarettes—which have a nearly universal standard for size, are sold in packs of 20, and are single-use—vaping products vary substantially. Perhaps the most notable divide in vaping products is between single-use products, often called closed systems, and open-system vaping devices that are reused by consumers refilling the device with e-liquid or vaping pods.

Closed-system or disposable vaping devices are designed to be thrown away after use. Once the vaping liquid is depleted or the battery loses its charge, the entire device is discarded. Unlike rechargeable and open-system vaping devices, closed-system vaping products do not require any maintenance or refilling.

In part because of their ease of use and portability, disposable vaping product popularity grew, eventually taking over open-system products as the market leader by 2022 , even though most products with MGOs were open systems.

States use a variety of designs to tax vaping products. Some states tax based on manufacturer, wholesale, or retail price; other states tax based on product, volume, or number of cartridges; while other states apply a bifurcated system with different rates for open- and closed-tank systems.

To test whether illicit vaping products are being taxed, we collected data on average retail prices of several vaping products for all 50 states and Washington, DC (from Management Science Associates Inc., corroborated by hand data collection across multiple states). We then calculated the tax that would be charged to each product in each state and analyzed the correlation between tax and price, hypothesizing that the excise taxes applied to vaping products would affect market prices for the taxed products, a well-documented phenomenon across various products.

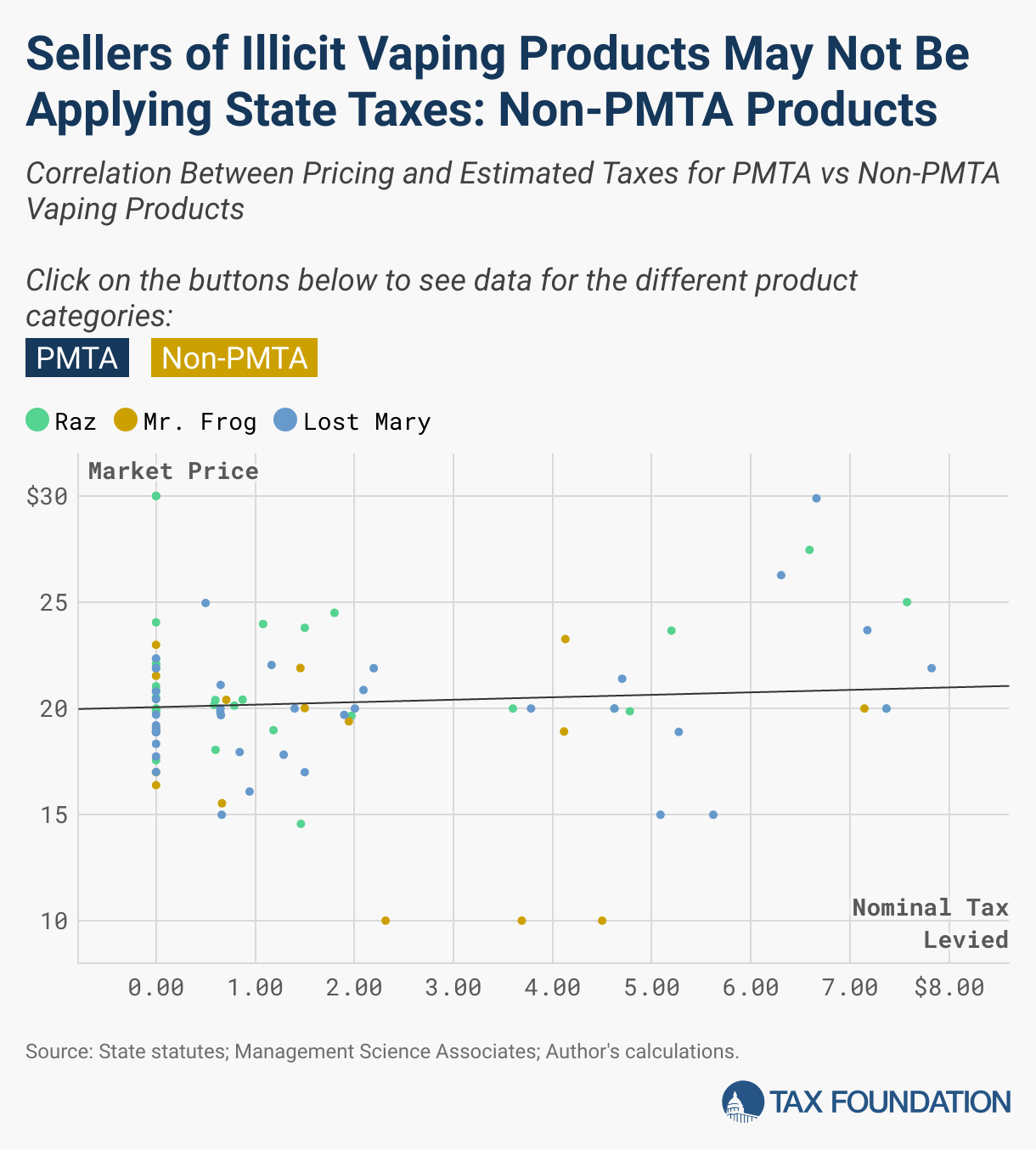

We find that legal products—those for which the FDA has granted marketing orders, or products that have pending litigation regarding their PMTA—had prices that were strongly correlated to the tax charged on their products. The average correlation for PMTA products was roughly 80 percent.

Chinese imports and other products without a PMTA, on the other hand, are a different story entirely. The average correlation between price and tax was only 33 percent. Some products displayed no relationship between price and tax, and a few products even displayed a negative relationship.

Figure 2 displays the market prices (vertical axis) and tax estimates (horizontal axis) for select vaping products. Column 1 displays products with a PMTA or a legally disputed PMTA application—Juul, NJOY, and Vuse. Column 2 displays small-market or Chinese products for which the FDA hasn’t granted a PMTA—Lost Mary, Raz, and Mr. Fog.

The products in the first column look as we would expect—a line of best fit with a close to unitary positive slope. The products in the second column don’t look the way we would expect if the state taxes were being incorporated into the price. In other words, these data suggest sellers of illicit products may not be applying state tax rates to vaping products.

What Can Be Done?

Legal vaping products are harm reduction tools for many existing smokers. Vapor products deliver nicotine to users without the combustion and inhalation of tar inherent to traditional cigarettes. While more research into the long-term harm-reduction potential of vapor products is needed, the present consensus is that vapor products are significantly less harmful than traditional combustible tobacco products. The English Ministry for Health concluded that vaping is 95 percent less harmful than smoking cigarettes.

This is why the FDA-induced disaster that has become the vaping market is such a tragedy. Instead of having a thriving, well-regulated, and taxed vaping industry, the FDA has handed control of the vaping market to illicit Chinese operators.

The good news is that the fix is easy. A two-pronged approach of better enforcement and quicker, broader FDA product approvals can quickly correct the US vaping market.

The FDA has increased enforcement on illicit products being sold in the United States, but there is still more work to do to enforce current regulations. Further, the government cannot rely solely on enforcement of prohibitions. Harm-reducing vapor products must face lower regulatory barriers to enable their competition with illicit vaping products and with legal combustible cigarettes to maximize their potential to improve public health.

One potential ally on the enforcement front could come from state departments of revenue and tax enforcement agencies. Our evidence on tax evasion of illicit products, largely Chinese imports, is only suggestive. State revenue departments could collect better microdata on vaping sales to determine if taxes are being properly charged, collected, and remitted. State agencies may have more enforcement options at their discretion and better tools to identify illicit operations.

Finally, the market approval process is too cumbersome, lengthy, and lacks transparency. The FDA Center for Tobacco Products acknowledged these faults and has started improving the PMTA process. The approval of the first flavored tobacco vaping products is a major step in the right direction. However, the process still lacks clarity and the timeline for an FDA decision is unacceptably long.

Given the FDA’s demonstrated inability to efficiently operate a premarket approval process, policymakers should consider reversing the order for approving marketing nicotine products for sale in the US. Under this system, products could be marketed and sold by default and only prohibited if the FDA provided scientific evidence, with a well-defined criterion approved by Congress.

It is also possible that the Supreme Court will weigh in. A vaping case, Wages and White Lion (Triton) v. FDA, is set to be considered next term. Previously, courts have relied partially on Chevron deference to rule against vaping businesses, but with the Court recently overturning this doctrine in favor of a lower standard of deference, there is potential for judicially mandated modifications to the regulatory process. Policy change is necessary to fix the US vaping market, but if not possible through legislative changes, the court system may mandate important corrections.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Share