Products You May Like

At the end of 2025, the individual taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

provisions in the Tax Cuts and Jobs Act (TCJA) expire all at once. Without congressional action, most taxpayers will see a notable tax increase relative to current policy in 2026.

In 2026, business taxes will also be higher as 100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs.

continues to phase down and TCJA base broadeners like research and development (R&D) amortization and a tighter limit on interest deductions remain in effect.

Policymakers may consider extending the current TCJA policy for individual tax provisions and canceling the business tax hikes. Tax Foundation estimates that permanence for the individual and business provisions (excluding the estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs.

changes) would cost about $3.8 trillion over the 10-year budget window from 2025 through 2034.

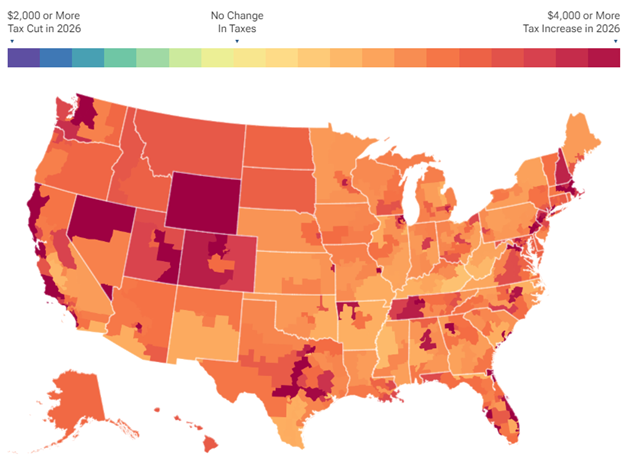

To visualize what’s at stake, Tax Foundation has estimated the average change in taxes paid per taxpayer under TCJA expiration relative to current policy across each congressional district. The congressional district map below shows the tax increase households will face if TCJA individual tax provisions expire and business taxes increase as scheduled.

The tax hikes from TCJA expiration would vary across the United States. The largest average tax hikes would be experienced by taxpayers who reside in California’s congressional districts. For example, the congressional district covering the San Francisco area would see an average tax hike of $16,127 per taxpayer, the highest in the U.S.

By contrast, northern New York City would see an average tax increase of $807 per taxpayer under TCJA expiration. Across all congressional districts, the average tax increase costs each taxpayer about $2,853 compared to current policy where TCJA remains in place and the business tax hikes are canceled.

Individual tax provisions also exhibit geographic variation. For example, the $10,000 cap on state and local tax (SALT) deductions tends to have the greatest impact on taxpayers in higher tax localities on the coasts of the U.S.

Tax Foundation estimates permanence for TCJA would create about 904,000 full-time equivalent jobs, ranging from more than 136,000 jobs in California and 75,000 jobs in Texas to about 1,660 new jobs in Vermont.

The resulting increase in employment would otherwise not occur if the TCJA is allowed to expire as scheduled in 2026 or is not made permanent. The map provides a state-level breakdown of the full-time equivalent jobs that would be lost if the TCJA individual provisions are not made permanent and the domestic TCJA-related business tax hikes are not canceled. In other words, it illustrates the potential job gains forfeited by allowing the TCJA to expire rather than be made permanent.

The choice to let TCJA provisions expire or to extend them will also forfeit broader economic gains. Making the TCJA individual tax provisions permanent and canceling TCJA-related business tax hikes would raise long-run GDP by about 1.1 percent, increase wages by about 0.3 percent, and create a 0.9 percent larger national capital stock.

The Impact Of TCJA Expirations By Congressional District, 2026

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Methodology

We estimate the geographic distribution of tax changes under an extension of the TCJA individual provisions and cancellation of domestic business provisions using conventional revenue estimates at the national level generated by the Tax Foundation’s General Equilibrium Model. In this map, we do not include the impact of making permanent the TCJA’s estate tax changes.

We then allocate to filers in congressional districts using data from the IRS Statistics of Income for individual tax returns in 2021. (Conventional revenue estimates do not include impacts on GDP and other economic aggregates.) The IRS data provides various tax characteristics broken down by congressional district (CD). For consistency with the latest SOI data, we use CDs as they existed in 2021, which may not map onto existing CDs due to redistricting.

From the IRS data, certain tax characteristics are used to allocate to CDs the conventional national revenue estimates for each of the TCJA provisions, as described in Table 2, and then averaged by the number of filers in each CD. This analysis’s accuracy is limited by the extent of the IRS data at the CD level.

For the TCJA business provisions, we assume these fall partly on capital income and partly on labor income, in accordance with several studies. In particular, we assume the corporate tax is initially borne mainly by capital income (90 percent in the first year), and over time the burden shifts to labor income until it is evenly split across capital and labor income in the long run (50 percent capital income and 50 percent labor income in the fifth year and beyond).

Our state-level jobs impacts are allocated based on the national jobs estimated from the Tax Foundation General Equilibrium Model and the distribution of labor and capital income across the states.

Share