Products You May Like

Key Findings

- A year since the global tax deal was agreed to by more than 130 countries, progress on implementing legislation has hit a lull.

- Implementation of the minimum tax rules is not expected until the end of 2023 or in 2024.

- Since the 2017 U.S. tax reforms and other recent international rules changes, onshoring of intellectual property (IP) to the U.S. has increased and outward investment strategies for U.S. companies have shifted. This should impact how the U.S. approaches the global tax deal.

- The international tax reforms included in the Build Back Better Act (BBBA) do not line up with the global minimum tax model rules and could prove a complex mess if adopted.

- Congress should prioritize evaluation of recent international tax trends and the model rules and adjust U.S. rules in a way that supports investment and innovation and moves towards simplicity.

Table of Contents

Related Content

Introduction

It has been a year since more than 130 countries signed up to an outline for international tax reform.[1] That outline described ambitious proposals to change the taxation of large multinational corporations with a shift in their tax base toward market countries alongside a global minimum tax. The two pieces, known as Pillar 1 (the shift in the tax base) and Pillar 2 (the global minimum tax), will impact the way large businesses arrange their tax affairs and the way governments design their tax policies.

International tax rules in the U.S. were overhauled as part of the Tax Cuts and Jobs Act (TCJA) in 2017. The changes shifted how U.S. companies structure their investments abroad and have led to onshoring of intellectual property (IP).

Now, Democratic policymakers are working on new reforms intended to change the 2017 rules to roughly align with the global tax deal. One problem with their approach, however, is that it was premature. The House of Representatives passed the Build Back Better Act (BBBA) in the fall of 2021, but model rules for the global minimum tax were not released until December 2021. The differences between the BBBA and the model rules could leave taxpayers (and the IRS) stuck in a challenging web of conflicting rules.

At this moment of global tax reform, U.S. policymakers should make decisions that provide a principled set of rules for multinational companies with a connection to the U.S. economy. Contrary to the current approach embodied in the BBBA, a strategic adjustment of U.S. tax rules could avoid a complex mess for taxpayers while ensuring the U.S. continues to be an attractive place for investment.

The global tax reform project has stalled somewhat. Rather than having the minimum tax rules in place in early 2023, it now looks like December 31, 2023, is the earliest date other major jurisdictions are aiming for implementing the rules.[2]

The delay provides U.S. lawmakers with time. There is no need to rush through a significant re-write of current U.S. cross-border rules. The past year has resulted in many new questions and few answers on how the global minimum tax might work. Congress should focus next steps on:

- Evaluating the performance of current U.S. cross-border rules;

- Observing how other jurisdictions plan to implement the global minimum tax; and

- Designing U.S. reforms with an eye toward simplicity, administrability, and compatibility with the global minimum tax.

This paper provides a framework for the next steps.

Evaluating the TCJA International Rules

The first global minimum tax was adopted by the U.S. as part of the TCJA. The policy, the tax on Global Intangible Low-Tax Income (GILTI), was just one part of the reforms that changed the incentives for where multinationals invest or hold their assets. Other important reforms included the reduction in the federal corporate tax rate from 35 percent to 21 percent, an incentive for holding IP within the U.S. (the Foreign Derived Intangible Income or FDII), and a disincentive for cross-border cost shifting (the Base Erosion and Anti-abuse Tax or BEAT). [3]

The TCJA international reforms broadened the U.S. tax base in several ways.

First, GILTI expanded the scope of U.S. companies’ foreign profits that face additional tax by the U.S. on an annual basis. Prior to TCJA, companies could opt to defer U.S. tax liability on their foreign earnings until the earnings were repatriated. Following the TCJA, foreign profits face at least a 10.5 percent minimum tax rate from GILTI, and foreign earnings can be repatriated without an additional toll tax.

In the three years immediately following passage of the TCJA (2018-2020), companies repatriated $1.54 trillion in foreign earnings. That is a dramatic increase relative to the three years leading up to tax reform (2015-2017), when $500 billion was repatriated.[4]

In many cases the tax rate companies face under GILTI is 13.125 percent or higher. The higher rate is because foreign tax credits are limited to 80 percent of their value and some domestic expenses are required to apply to foreign earnings. The combined tax (foreign taxes plus U.S. taxes) on the U.S. share of foreign profits was recently estimated by Tax Foundation economist Cody Kalen to be 19.3 percent.[5] By design, GILTI has changed the incentives for investing in foreign low-tax jurisdictions because the floor for foreign tax rates is no longer zero.

A working paper by economists Matthias Dunker, Max Pflitsch, and Michael Overesch examines how GILTI impacted incentives for companies to acquire businesses in foreign low-tax jurisdictions. Compared to companies not impacted by GILTI, they find that GILTI-affected firms have been less likely to merge with or acquire foreign companies in low-tax locations.[6] Similarly, research by academic accountants Harald Amberger and Leslie A. Robinson suggests the TCJA reforms reduced the amount of tax-motivated cross-border acquisitions by U.S. firms.[7]

The second way TCJA broadened the tax base was via FDII, which was designed to provide a lower tax rate of 13.125 percent on profits from exports related to IP held within the U.S. The goal of the lower tax rate was to incentivize businesses to keep their software, patents, or copyrights in the U.S. rather than offshoring them to a foreign low-tax jurisdiction.

When IP assets are held offshore, the U.S. tax base only benefits to the extent that GILTI or other rules addressing tax avoidance apply. When IP assets are in the U.S., the IRS has the primary right to tax related earnings. In 2017 and 2018, companies imported $200 million in IP assets from foreign affiliates.

Together, the policies (along with changes adopted by foreign jurisdictions) have had a significant impact on where U.S. companies hold their foreign assets and where they hold their IP.[8] Two indicators summarize the impact.

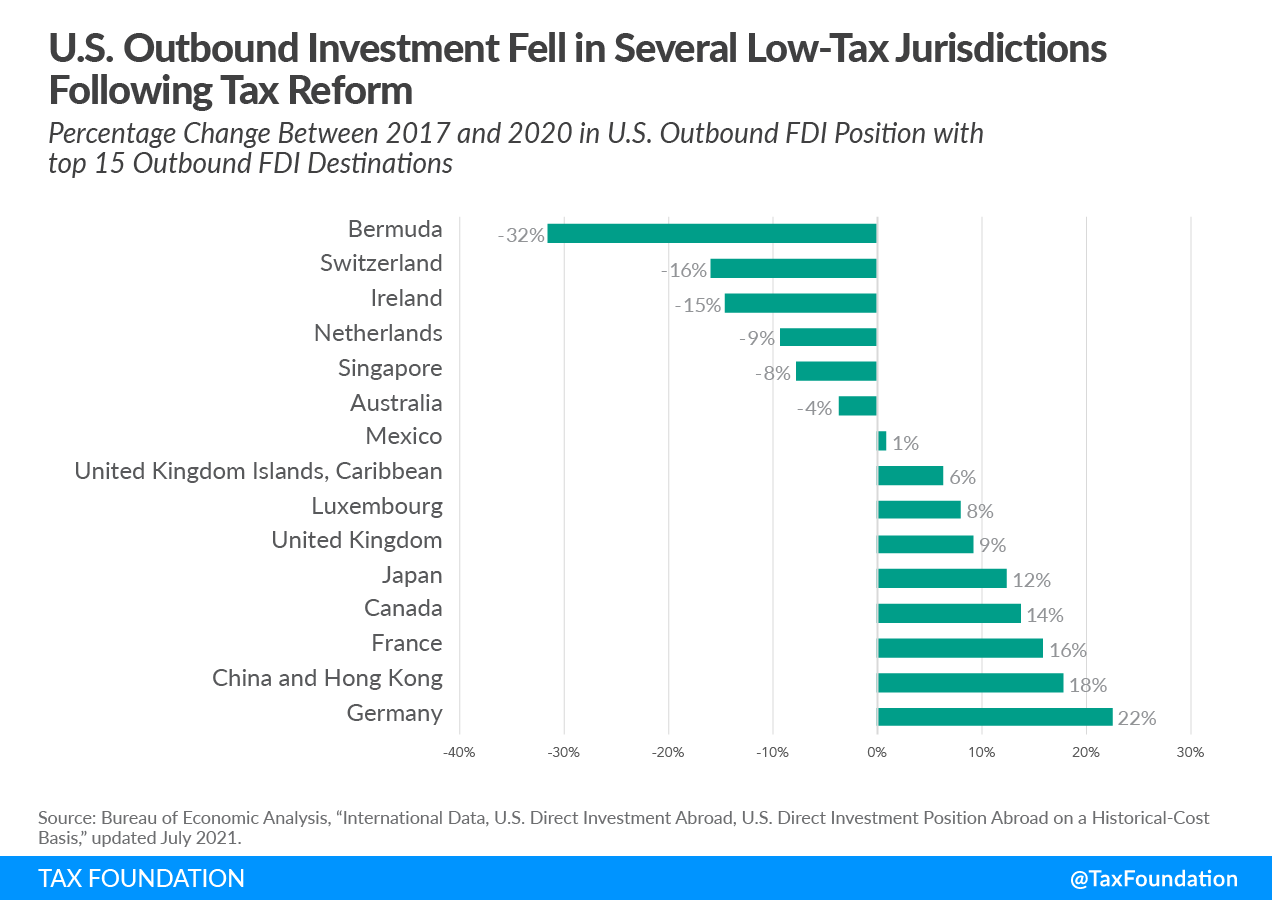

The first indicator is the destination for outbound Foreign Direct Investment (FDI) from the U.S. U.S. businesses often rely on foreign low-tax jurisdictions when they expand abroad, which can either be the destination for an expanded foreign operating base or a conduit through which investment flows to another jurisdiction.

Between 2017 and 2020 (the latest available data), the level of U.S. outbound investment in the top 15 destinations for FDI has changed significantly while the overall level of outbound FDI remained roughly flat. U.S. outbound investment fell in Bermuda (-32 percent), Switzerland (-16 percent), and Ireland (-15 percent). Meanwhile outbound investment rose in Germany (22 percent), China (18 percent), Canada (14 percent), and Japan (12 percent). The shift suggests U.S. companies have been rotating their investments away from lower-tax jurisdictions to higher-tax countries since the TCJA was signed into law.

A second indicator is exports of IP services to foreign jurisdictions, particularly to Ireland. For tax reasons, many U.S. companies have deployed investments in Ireland as part of their corporate structure and investment strategy in recent decades. Prior to 2020, they also regularly used entities in the Netherlands and a zero-tax jurisdiction to minimize the amount of taxes paid on profits from IP.[9]

Since 2020, however, such strategies are no longer viable, and many U.S. companies have brought IP back to the U.S. to serve Irish (and other) markets with IP held in the U.S. Since the start of 2020, U.S. exports of IP services to Ireland have skyrocketed.

By the end of 2021, Irish entities had imported €142.5 billion (US $150.3 billion) in IP services from the U.S.—more than double the total imports from 2010 to 2017.

Recent research by economists Javier Garcia-Bernardo, Petr Janský, and Gabriel Zucman shows the driving force behind a reduction in the share of profits that U.S. companies book abroad was repatriations of IP.[10]

As trends continue to develop, U.S. policymakers should study them to understand how the TCJA reforms affect the taxes paid by U.S. multinationals, the destination for U.S. outbound investment, and the location of IP.

Observing Other Jurisdictions

In the fall of 2021, the Build Back Better Act (BBBA) passed through the House of Representatives. Changes to GILTI, FDII, and BEAT were all included in the package. Some of the proposals would have improved the way the policies work relative to current law, primarily related to GILTI provisions that would limit the amount of domestic expenses allocated to foreign profits.

A major challenge for legislators at the time was that the model rules for the global minimum tax had not yet been released. If U.S. legislators had the model rules in hand when designing the provisions of the BBBA, it is likely they would have made different choices.

Now, however, because of the lull in activity to implement the rules, U.S. lawmakers have a chance to pause and explore the model rules while observing how other jurisdictions might implement the global minimum tax. This should provide lessons for a different approach for U.S. policy than what is included in the BBBA.

The Model Rules and the Build Back Better Act

The model rules for the global minimum tax were released in December 2021.[11] Further commentary and examples of how the rules might apply were released in March 2022.

The global minimum tax establishes a 15 percent effective tax rate based on the financial accounts of large corporate entities on a jurisdiction-by-jurisdiction basis. Under the minimum tax, a company would need to calculate the effective tax rate their operations face in each jurisdiction where they have profits. After normal corporate income taxes and taxes paid under controlled foreign corporation rules are accounted for, a top-up may be assessed to ensure the effective tax rate in a jurisdiction is at 15 percent. A substance-based income exclusion is provided both for a share of tangible assets and payroll.

The rules also use a global revenue threshold of €750 million ($790 million) in at least two of the previous four fiscal years with an optional exclusion for entities in a jurisdiction with average revenues below €10 million ($10.55 million) or income less than €1 million ($1.05 million) (the average is calculated using the current year and two previous years). The thresholds determine whether a company needs to comply with the rules in general or in a specific jurisdiction.[12]

The rules lay out four tools for implementing top-up taxes on low-taxed income. Generally, the first three rules apply to the same definition of taxable income, but they differ in which jurisdiction might apply the rule and where a multinational might send its tax payment for the top-up.

The three main rules of the global minimum tax are as follows:

- Qualified Domestic Minimum Top-up Tax (QDMTT): Applies to low-tax profits within a jurisdiction’s own borders.

- Income Inclusion Rule (IIR): Applies to low-tax profits of foreign subsidiaries of a jurisdiction’s own companies.

- Under-taxed Profits Rule (UTPR): Applies to low-tax profits of a subsidiary of a foreign company that has low-tax profits that are not taxed under the other top-up rules.

A fourth rule based in tax treaties is the Subject to Tax Rule (STTR), which a country could use to apply a 9 percent tax on payments to related parties taxed below that rate.

The three main rules of the global minimum tax only roughly correspond to proposals in the BBBA passed by the House of Representatives in 2021. For example, the proposed changes to GILTI would not match the tax base of the minimum tax rules as they do not use financial accounting. The substance-based income exclusion would only apply to tangible assets rather than payroll. Additionally, the effective tax rate calculation for GILTI includes a limit on foreign taxes paid (95 percent in the BBBA; current law only provides an 80 percent credit). The per-country effective rate could be 15.8 percent or higher under the BBBA version of GILTI.

The differences, alongside the complexities of U.S. foreign tax credit rules, create significant gaps between the BBBA and the global minimum tax model rules.

To avoid a potentially chaotic and confusing adaptation of the minimum tax approach, U.S. lawmakers should consider how other jurisdictions are exploring implementation strategies.

| Current Law | Scheduled Change to Current Law | Build Back Better Act | President Biden’s Budget | Global Minimum Tax Model Rules | |

|---|---|---|---|---|---|

| Effective Date | 1/1/2018 | 1/1/2026 | 1/1/2023 | 12/31/2024 | 2023 (12/31/2023 for the EU and UK) |

| Rate | 10.5% (could be 13.125% or higher depending on exposure to foreign taxes) | 13.125% (could be 16.4% or higher depending on exposure to foreign taxes) | 15% (could be 15.8% or higher depending on exposure to foreign taxes) | 20% (could be 21.1% or higher depending on exposure to foreign taxes) | 15% |

| Exclusion for a Normal Return on Tangible Assets | 10% deduction for foreign tangible assets | 10% deduction for foreign tangible assets | 5% deduction for foreign tangible assets | Assumes that Build Back Better becomes law | 8% incrementally reduced to 5% over the first five years |

| Exclusion for a Normal Return on Payroll Costs | No | No | No | 10% incrementally reduced to 5% over the first five years | |

| Loss Carryovers | No | No | No | Included in Deferred Tax Asset | |

| Foreign Tax Treatment | Credit for 80% of foreign taxes paid, no carryover for excess credits | Credit for 80% of foreign taxes paid, no carryover for excess credits | Credit for 95% of foreign taxes paid, 5-year carryforward of excess foreign tax credits | Deferred Tax Asset recast at 15% rate | |

| Jurisdictional Calculation | Foreign income is blended together | Foreign income is blended together | Country-by-country | Country-by-country | |

| Threshold for Application | None, 10 percent ownership threshold | None, 10 percent ownership threshold | None, 10 percent ownership threshold | €750 million ($790 million) in global revenues | |

| Income Definition | Foreign taxable income as defined in the Internal Revenue Code, no use of financial accounting methods | Foreign taxable income as defined in the Internal Revenue Code, no use of financial accounting methods | Foreign taxable income as defined in the Internal Revenue Code, no use of financial accounting methods | Financial profits as defined by accounting standards and adjusted to align closer to taxable profits | |

| Under-taxed Profits Rule (UTPR) | Base Erosion and Anti-Abuse Tax (not comparable to the OECD model rules) | Base Erosion and Anti-Abuse Tax (not comparable to the OECD model rules) | Base Erosion and Anti-Abuse Tax (not comparable to the OECD model rules) | Yes, replacing BEAT | Yes |

| Qualified Domestic Minimum Top-up Tax | None | None | 15 percent alternative minimum tax on worldwide financial profits (not comparable to the OECD model rules) | Yes, only applied when a UTPR applies to a U.S. company; also includes the 15 percent alternative minimum tax on worldwide financial profits (not comparable to the OECD model rules) | Yes |

| Sources: U.S. Congress, “H.R. 1 An Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018,” Dec. 22, 2017, https://www.congress.gov/bill/115th-congress/house-bill/1/text; Joint Committee on Taxation, “Estimated Budget Effects of the Conference Agreement for H.R. 1, The ‘Tax Cuts and Jobs Act,’” Dec. 18, 2017, https://www.jct.gov/publications/2017/jcx-67-17/; U.S. Congress, “H.R. 5376 Build Back Better Act,” Nov. 19, 2021, https://www.congress.gov/bill/117th-congress/house-bill/5376; Alex Durante et al, “House Build Back Better Act: Details & Analysis of Tax Provisions in the Budget Reconciliation Bill,” Tax Foundation, Dec. 2, 2021, https://www.taxfoundation.org/build-back-better-plan-reconciliation-bill-tax/; OECD, “Tax Challenges Arising from the Digitalisation of the Economy – Global Anti-Base Erosion Model Rules (Pillar Two),” Dec. 20, 2021, https://www.oecd.org/tax/beps/tax-challenges-arising-from-the-digitalisation-of-the-economy-global-anti-base-erosion-model-rules-pillar-two.htm; Department of the Treasury, “General Explanations of the Administration’s Fiscal Year 2023 Revenue Proposals,” March 2022, https://home.treasury.gov/system/files/131/General-Explanations-FY2023-Table.pdf. | |||||

How Other Jurisdictions Are Approaching the Model Rules

Across the world, several jurisdictions have released consultation papers and policy documents outlining questions and options for implementing the global minimum tax rules.

While the European Union directive on the minimum tax is furthest along in the legislative process, progress has stalled as concerns from Poland, and more recently Hungary, have kept the directive from moving forward. The EU Council hopes to get unanimous agreement on the proposal and then the process of implementation in the 27 member countries could begin. The current proposal suggests implementation by December 31, 2023.

Several other jurisdictions have been exploring whether to adopt all the global minimum tax rules or a subset of the rules. Switzerland and the United Arab Emirates are considering adjustments to their corporate income taxes to increase the effective tax burden on companies before the global minimum tax calculations are begun. New Zealand’s approach seems focused on ensuring any low-tax profits that could be taxed by New Zealand under the global minimum tax are captured by their approach to implement the rules.

| Jurisdiction | Summary | Potential Timeline for Adoption |

|---|---|---|

| Canada | Considering implementation of the QDMTT, but likely to adopt IIR and UTPR in line with the model rules. | Expected implementation date in 2023; UTPR implementation delayed to 2024. |

| European Union | Proposal includes QDMTT, IIR, and UTPR to be adopted by all 27 EU member states. | Rules are to be implemented as of Dec. 31, 2023; UTPR to be applied in 2024. Countries that have no more than 12 companies that would be subject to the rules could delay implementation for 6 consecutive years following December 31, 2023. |

| Ireland | Likely to follow adoption of the EU directive with domestic legislation. | Following the EU timeline. |

| Jersey | Exploring roughly 3 options including no adoption of minimum tax rules, implementation of IIR and/or UTPR, introduction of QDMTT. | Legislative process may take place in 2022 in order for rules to be applied in 2023. |

| New Zealand | Still considering whether to adopt the global minimum tax rules; decision will depend on whether a critical mass of countries adopt the rules, and focus will be allowing New Zealand to tax under-taxed profits rather than another jurisdiction. | If the government chooses to adopt the rules, the legislation would likely be adopted in 2023. |

| Switzerland | Proposal to adopt additional tax measures at the Cantonal level to cover the difference between the top-up taxes and current tax levels. | A constitutional change will be required to allow differential taxation of large companies. New rules could potentially be in force by Jan. 1, 2024. |

| United Arab Emirates | Adopting a 9 percent domestic corporate income tax on adjusted accounting net profit exceeding AED 375,000 ($102,000). | To be applied to financial years beginning after June 1, 2023. |

| United Kingdom | Considering implementation of the QDMTT, but likely to adopt IIR and UTPR in line with the model rules. | Expected implementation date of Dec. 31, 2023; UTPR implementation delayed to 2024. |

| Source: Department of Finance Canada, “Budget 2022: A Plan to Grow Our Economy and Make Life More Affordable,” April 2022, https://www.budget.gc.ca/2022/home-accueil-en.html; Council of the European Union, “Draft Council Directive on ensuring a global minimum level of taxation for multinational groups in the Union, Presidency Compromise Text,” June 16, 2022, https://data.consilium.europa.eu/doc/document/ST-8779-2022-INIT/en/pdf; Ireland Department of Finance, “Public Consultation on Pillar Two Minimum Tax Rate Implementation,” May 26, 2022, https://www.gov.ie/en/consultation/c68e4-public-consultation-on-pillar-two-minimum-tax-rate-implementation/; Government of Jersey, “OECD Pillars 1 & 2: tax policy reflections,” April 2022, https://www.gov.je/SiteCollectionDocuments/Tax%20and%20your%20money/R%20OECD%20Pillars%201%20and%202%20tax%20policy%20reflections.pdf; New Zealand Inland Revenue, “OECD Pillar Two: GloBE rules for New Zealand,” May 5, 2022, https://www.taxpolicy.ird.govt.nz/publications/2022/2022-ip-oecd-pillar-two; Switzerland Bundesrat, “Bundesrat eröffnet Vernehmlassung zur Umsetzung der OECD/G20-Mindestbesteuerung,” Mar. 11, 2022, https://www.admin.ch/gov/de/start/dokumentation/medienmitteilungen.msg-id-87569.html; Federal Tax Authority, “UAE Corporate Tax,” United Arab Emirates, Jan. 31, 2022, https://tax.gov.ae/FTATacsoft5CMS/DataFolder/Images/corporatetax/corporatetax_en.jpg; HM Treasury, “OECD Pillar 2 – Consultation on Implementation,” Jan. 11, 2022, https://www.gov.uk/government/consultations/oecd-pillar-2-consultation-on-implementation. | ||

{kind=link}

The various approaches around the world suggest U.S. lawmakers should also consider taking time to evaluate options beyond the BBBA to implement the global minimum tax, and plenty of time is available to determine the right course of action.

The Build Back Better Act and the U.S. Tax Base

The intersection between the global minimum tax rules and the Build Back Better Act (BBBA) reforms has significant implications for the U.S. tax base. Under the model rules, the taxable income of a large multinational will be taxed through five layers of rules with each consecutive layer depending on how much tax is collected under the previous one:

- Normal corporate income taxes in the jurisdiction where income is earned;

- Controlled Foreign Corporation (CFC) rules applied by the jurisdiction of a company’s headquarters or owners;

- Qualified Domestic Minimum Top-up Tax (QDMTT) applied by the jurisdiction where low-tax earnings arise;

- Income Inclusion Rule (IIR) applied by the jurisdiction of a company’s ultimate parent entity on low-tax foreign earnings in each foreign jurisdiction where the company has low-tax earnings; and

- Under-taxed Profits Rule (UTPR) applied to entities within a jurisdiction on a country’s share of low-tax profits of the corporate group that have not already been taxed by one of the previous four rules.

The U.S. currently has rules in place for number 1 and number 2. The U.S. corporate income tax applies at a federal level with a 21 percent rate with various deductions and credits that can result in effective tax rates below 21 percent. The U.S. also has CFC rules that apply to foreign income of U.S. multinationals in certain circumstances. The U.S. Treasury has interpreted the model rules as including the current law version of GILTI as a CFC rule.[13] Credits for foreign taxes paid can be applied to reduce additional U.S. tax liability, although they are limited to 80 percent of their value for GILTI, and recent regulatory changes have narrowed the scope of creditable foreign taxes.

Taken together, current U.S. law provides the U.S. with the first two opportunities to collect revenue from the taxable income of a large U.S. multinational: first in line on the U.S. corporate income tax base and second in line (behind foreign corporate taxes) on a U.S. company’s foreign income tax base.

After paying U.S. domestic corporate income tax and GILTI, if a U.S. company has income taxed at below the global minimum tax effective rate of 15 percent, then the other global minimum tax rules come into play, including a foreign QDMTT.

Tax credits provided to U.S. companies for clean energy initiatives, research and development, or deductions connected to FDII expose the tax base of a U.S. company to being taxed by a foreign jurisdiction under the UTPR.[14]

If other jurisdictions begin adopting the global minimum tax rules, current law means the U.S. domestic tax base is exposed to foreign taxes on earnings which are low-tax by design according to U.S. tax incentives for clean energy and innovative activities.

The BBBA approach, however, could prove to be even worse than current law.

Instead of taking the second place in the list above, moving to the BBBA version of GILTI would make the U.S. tax on foreign earnings of U.S. companies fall back in line to fourth position as GILTI becomes an IIR rather than its current role as a CFC rule.

The U.S. would be giving up the tax base it currently taxes using GILTI. In fact, the rules incentivize countries to adopt QDMTTs that would apply ahead of IIRs. Research by economists Michael Devereux, John Vella, and Heydon Wardell-Burrus suggests some jurisdictions may prefer to collect corporate taxes through the QDMTT than even the traditional corporate tax.[15]

Tax Foundation modeling suggests if enough foreign jurisdictions adjust their corporate income taxes to collect low-tax earnings within their jurisdictions, then aligning GILTI with the global minimum tax would result in a net loss of U.S. federal tax revenue.[16]

The BBBA would also leave in place many tax incentives that expose low-tax profits in the U.S. to a foreign country’s UTPR. The tax benefits provided by the U.S. tax code would be surrendered to other countries in the form of additional tax revenues to foreign jurisdictions.

So, if the BBBA is adopted, then the U.S. moves down the food chain for taxing foreign profits of U.S. multinationals (behind foreign QDMTTs), and the U.S. domestic tax base remains exposed to the UTPR.

Additionally, the structure of the BBBA GILTI rules is even more complex than the model rules for the global minimum tax. The complexity is primarily due to the structure of U.S. foreign tax credit rules. Companies would need to track foreign earnings, losses, and taxes paid in multiple categories for every jurisdiction where they have operations, likely leading to an explosion of enforcement challenges for the IRS and compliance headaches for U.S. companies.

As mentioned previously, the tax base for the BBBA version of GILTI is also different from the model rules. Even if other jurisdictions increase their taxes through higher corporate income tax rates or adoption of QDMTTs, GILTI might still apply due to its different structure and broader base.

Foreign companies that face just the global minimum tax rules would be at an advantage relative to U.S. companies due to relatively less complexity and a more straightforward tax burden in line with the model rules.

The weaknesses in the BBBA approach suggest a new approach is needed if U.S. tax rules are to support investment and innovation in the U.S.

Designing A Strategic Approach for U.S. Reforms

If adopting the changes to GILTI in the Build Back Better Act (BBBA) would be a strategic mistake when considering the model rules, then Congress should explore what might constitute a success.

The first goal should be to identify ways to simplify U.S. tax rules on foreign earnings. The foreign tax credit is an important place to start. The foreign tax credit connections between GILTI in current law and the BBBA contribute significantly to additional complexity for U.S. multinationals. And recently, the U.S. Treasury has promulgated regulations that have added even more uncertainty around the foreign tax credit in major ways.[17]

Congress should explore ways to consolidate the multiple foreign tax credit baskets to simplify filing and tracking requirements. Tax lawyers Robert Culbertson and Michael Caballero recently proposed adopting a system that would treat foreign high-tax income and low-tax income separately.[18] This represents one path to avoid companies having to track credits for every jurisdiction.

If the model rules truly come into place around the world, fully replacing GILTI with a worldwide tax system and full creditability for foreign taxes could also prove simpler than the model rules or the BBBA approach.

A second goal should be to promote investment and innovation in the U.S. in ways that align with the model rules. To avoid having U.S. companies lose tax benefits to foreign UTPRs, Congress should review existing tax incentives most exposed to the UTPR and prioritize them for reform or elimination. Additional revenues from eliminated tax incentives could be used to extend investment-friendly policies that comply with the global minimum tax such as full expensing for capital investment.[19]

The U.S. should also maintain a relatively low corporate tax rate consistent with the international agreement.

If the model rules do not become the new norm for cross-border taxation, the U.S. should improve on the reforms from 2017 by adopting a more simplified territorial system. A simplified approach could include removing the foreign tax credit haircut for GILTI and addressing the hidden tax embedded in expense allocation rules.[20]

Overall, taking a different approach from the BBBA would provide Congress a chance to simplify the taxation of foreign earnings and reform tax incentives in a way that supports investment within the U.S. without giving up significant control of the U.S. tax base to foreign jurisdictions.

Conclusion

A lot has changed in international tax rules over the last decade. The 2017 TCJA was only a part of it, and it would be worthwhile for Congress to take time to explore how new rules have impacted the U.S. tax base and the investment behavior of U.S. companies.

Policymakers should also take time to understand how other jurisdictions are planning to implement the global minimum tax to inspire discussion of a new, more strategic approach to changing U.S. international tax rules. The BBBA approach is flawed primarily because it was prematurely developed before the global minimum tax model rules were released.

The U.S. international tax system can be simplified even in the context of the global minimum tax. Such an achievement would require legislators to focus their efforts on designing rules that fit within the new framework and do not unnecessarily give up control of the U.S. tax base.

Congress has a chance to avoid a nearsighted, strategic mistake and instead develop rules in support of U.S. investment and innovation, and it should take that chance.

Launch U.S. International Tax Resource Center

[1] OECD/G20 Base Erosion and Profit Shifting Project, “Statement on a Two-Pillar Solution to Address the Tax Challenges Arising from the Digitalisation of the Economy,” OECD, July 1, 2021, https://www.oecd.org/tax/beps/statement-on-a-two-pillar-solution-to-address-the-tax-challenges-arising-from-the-digitalisation-of-the-economy-july-2021.pdf.

[2] This is the case for the United Kingdom and the European Union.

[3] For more information on the mechanics of these policies, see Kyle Pomerleau, “A Hybrid Approach: The Treatment of Foreign Profits under the Tax Cuts and Jobs Act,” Tax Foundation, May 2018, https://files.taxfoundation.org/20180502205047/Tax-Foundation-FF586.pdf.

[4] Bureau of Economic Analysis, “Table 4.2. U.S. International Transactions in Primary Income on Direct Investment, Receipts, Dividends and withdrawals,” Mar. 23, 2022.

[5] Cody Kallen, “How Heavily Taxed Are U.S. Multinationals?” Tax Foundation, Sept. 29, 2021, https://www.taxfoundation.org/us-multinational-corporations-tax/.

[6] Mathias Dunker, Max Pflitsch, and Michael Overesch, “The Effects of the U.S. Tax Reform on Investments in Low-Tax Jurisdictions – Evidence from Cross-Border M&As,” Nov. 3, 2021, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3932459&dgcid=ejournal_htmlemail_tax:ejournal_abstractlink.

[7] Harald J. Amberger and Leslie A. Robinson, “The Initial Effect of U.S. Tax Reform on Foreign Acquisitions,” WU International Taxation Research Paper Series 2020:06, Apr. 19, 2022, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3612783.

[8] Seamus Coffey, “The changing nature of outbound royalties from Ireland and their impact on the taxation of the profits of US multinationals – May 2021,” Ireland Department of Finance, June 14, 2021, https://www.gov.ie/en/publication/fbe28-the-changing-nature-of-outbound-royalties-from-ireland-and-their-impact-on-the-taxation-of-the-profits-of-us-multinationals-may-2021/.

[9] Ibid.

[10] Javier Garcia-Bernardo, Petr Janský, and Gabriel Zucman, “Did the Tax Cuts and Jobs Act Reduce Profit Shifting by US Multinational Companies?” National Bureau of Economic Research, WP 30086, May 2022, https://www.nber.org/papers/w30086.

[11] OECD, “Tax Challenges Arising from the Digitalisation of the Economy – Global Anti-Base Erosion Model Rules (Pillar Two),” Dec. 20, 2021, https://www.oecd.org/tax/beps/tax-challenges-arising-from-the-digitalisation-of-the-economy-global-anti-base-erosion-model-rules-pillar-two.htm.

[12] No such exclusion thresholds are available for U.S. companies under GILTI (current law or in the BBBA).

[13] EY, “Americas Tax Policy: This Week in Tax Policy for May 20,” May 22, 2022, https://taxnews.ey.com/news/2022-0809-americas-tax-policy-this-week-in-tax-policy-for-may-20.

[14] Daniel Bunn, “U.S. Tax Incentives Could be Caught in the Global Minimum Tax Crossfire,” Tax Foundation, Jan. 28, 2022, https://www.taxfoundation.org/us-global-minimum-tax-build-back-better/.

[15] Michael P. Devereux, John Vella, and Heydon Wardell-Burrus, “Pillar 2: Rule Order, Incentives, and Tax Competition,” Oxford University Centre for Business Taxation Policy Brief, Jan. 14, 2022, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4009002.

[16] See the second table in Daniel Bunn, “Adoption of Global Minimum Tax Could Raise U.S. Revenue…or Not,” Tax Foundation, Aug. 19, 2021, https://www.taxfoundation.org/us-global-minimum-tax-revenue/.

[17] Daniel Bunn, “A regulatory tax hike on US multinationals,” MNE Tax, Feb. 28, 2022, https://mnetax.com/a-regulatory-tax-hike-on-us-multinationals-46865.

[18] Robert E. Culbertson and Michael J. Caballero, “Rewriting the Foreign Tax Credit Limitation (Again),” Taxes: The Tax Magazine, March 2022, https://www.cov.com/-/media/files/corporate/publications/2022/03/rewriting-the-foreign-tax-credit-limitation-again.pdf.

[19] For more analysis of the connection between the global minimum tax and tax incentives see Table III.2 in UNCTAD, “World Investment Report 2022,” June 2022, https://unctad.org/system/files/official-document/wir2022_en.pdf.

[20] Cody Kallen, “Expense Allocation: A Hidden Tax on Domestic Activities and Foreign Profits,” Tax Foundation, Aug. 26, 2021, https://www.taxfoundation.org/expense-allocation-rules-hidden-tax-foreign-profits/.