Products You May Like

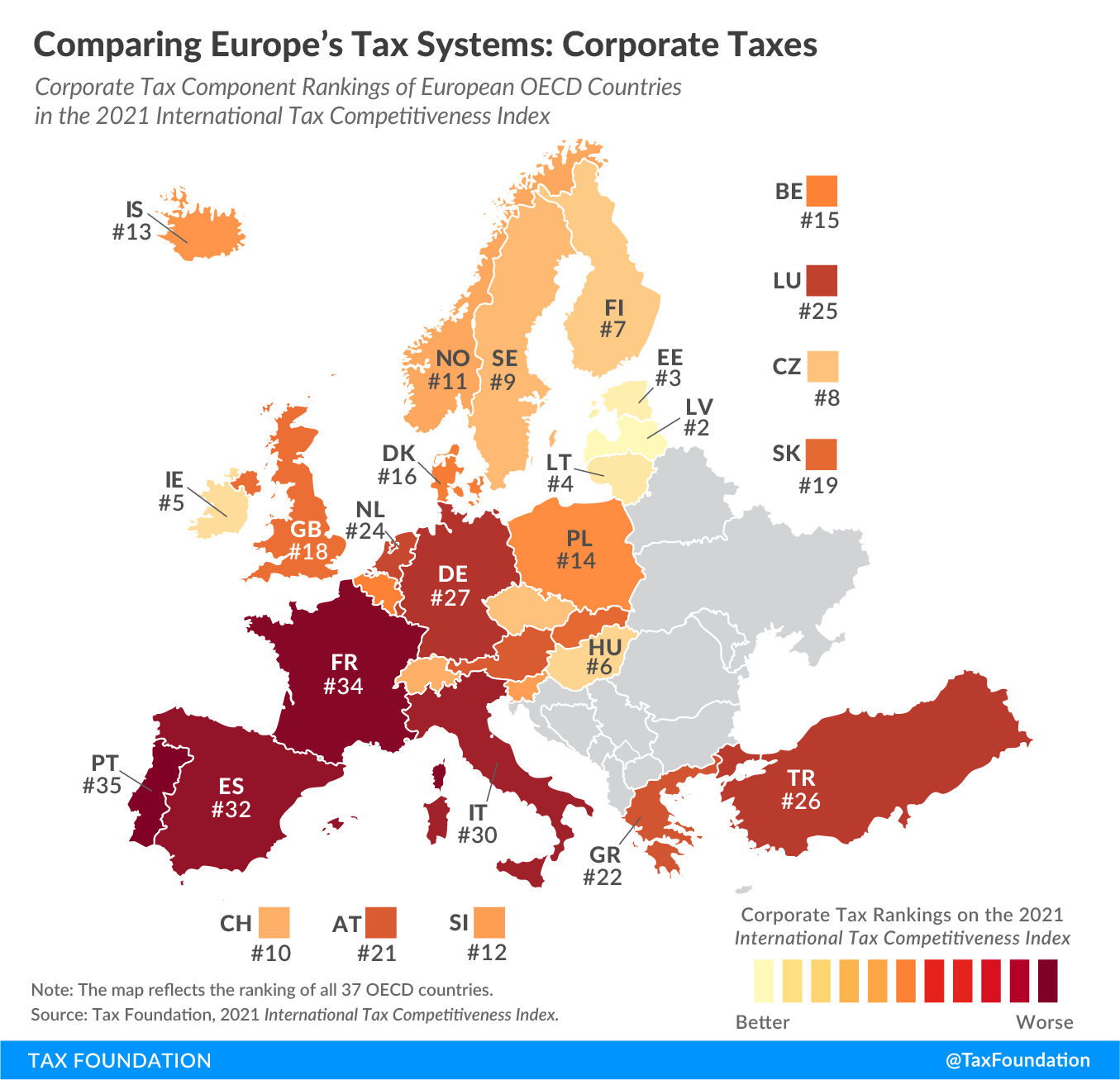

On October 17, we released the International Tax Competitiveness Index 2021, a study that measures and compares the competitiveness and neutrality of all 37 OECD countries’ tax systems. In the coming weeks, we will illustrate how European OECD countries rank in each of the five components of the Index: corporate income taxes, individual taxes, consumption taxes, property taxes, and the international tax system. Today we look at how European countries’ corporate income tax systems compare within the OECD.

Unlike other studies that compare tax burdens, the Index measures how well a country structures its tax code. A tax code that is competitive and neutral promotes sustainable economic growth and investment while raising sufficient revenue for government priorities. Our corporate income tax component scores countries not only on their corporate tax rates but also on how they handle net operating losses, capital allowances, inventory valuation, and allowances for corporate equity, whether and to what extent distortionary patent boxes and R&D tax incentives are granted, the application of digital services taxes, and on the complexity of the corporate income tax.

Click the link below to see an interactive version of OECD countries’ corporate tax rankings, then click on your country for more information about what the strengths and weaknesses of its tax system are and how it compares to the top and bottom five countries in the OECD.

Latvia and Estonia have the best corporate tax systems in the OECD. Both countries have a cash-flow tax on business profits. This means that profits only get taxed when they are distributed to shareholders. If a business decides to reinvest its profits instead of paying dividends to shareholders, there is no tax on such profits.

In contrast, Portugal has the least competitive and neutral corporate income tax system in Europe (Japan ranks the lowest in the OECD). At 31.5 percent, Portugal levies one of the highest corporate tax rates on business profits. Only limited net operating losses can be carried forward and carried back; purchases of machinery, buildings, and intangibles cannot be fully expensed.

To see whether your country’s corporate tax rank has improved in recent years, check out the table below. To learn more about how we determined these rankings, read our full methodology here.

| Corporate Tax Component of the International Tax Competitiveness Index between 2019 and 2021 (for all OECD countries) | ||||

|---|---|---|---|---|

| OECD Country | 2019 Rank | 2020 Rank | 2021 Rank | Change from 2020 to 2021 |

| Australia (AU) | 30 | 30 | 29 | 1 |

| Austria (AT) | 19 | 23 | 21 | 2 |

| Belgium (BE) | 20 | 10 | 15 | -5 |

| Canada (CA) | 22 | 21 | 23 | -2 |

| Chile (CL) | 32 | 5 | 1 | 4 |

| Czech Republic (CZ) | 36 | 37 | 37 | 0 |

| Denmark (DK) | 6 | 7 | 8 | -1 |

| Estonia (EE) | 15 | 16 | 16 | 0 |

| Finland (FI) | 2 | 2 | 3 | -1 |

| France (FR) | 7 | 8 | 7 | 1 |

| Germany (DE) | 37 | 36 | 34 | 2 |

| Greece (GR) | 28 | 28 | 27 | 1 |

| Hungary (HU) | 21 | 22 | 22 | 0 |

| Iceland (IS) | 5 | 6 | 6 | 0 |

| Ireland (IE) | 10 | 11 | 13 | -2 |

| Israel (IL) | 4 | 4 | 5 | -1 |

| Italy (IT) | 29 | 29 | 17 | 12 |

| Japan (JP) | 26 | 31 | 30 | 1 |

| Korea (KR) | 35 | 35 | 36 | -1 |

| Latvia (LV) | 33 | 33 | 33 | 0 |

| Lithuania (LT) | 1 | 1 | 2 | -1 |

| Luxembourg (LU) | 3 | 3 | 4 | -1 |

| Mexico (MX) | 25 | 25 | 25 | 0 |

| Netherlands (NL) | 31 | 32 | 31 | 1 |

| New Zealand (NZ) | 24 | 24 | 24 | 0 |

| Norway (NO) | 23 | 27 | 28 | -1 |

| Poland (PL) | 12 | 14 | 11 | 3 |

| Portugal (PT) | 13 | 15 | 14 | 1 |

| Slovak Republic (SK) | 34 | 34 | 35 | -1 |

| Slovenia (SI) | 16 | 17 | 19 | -2 |

| Spain (ES) | 11 | 12 | 12 | 0 |

| Sweden (SE) | 27 | 26 | 32 | -6 |

| Switzerland (CH) | 8 | 9 | 9 | 0 |

| Turkey (TR) | 9 | 13 | 10 | 3 |

| United Kingdom (GB) | 14 | 18 | 26 | -8 |

| United States (US) | 17 | 20 | 18 | 2 |

Was this page helpful to you?

Thank You!

The Tax Foundation works hard to provide insightful tax policy analysis. Our work depends on support from members of the public like you. Would you consider contributing to our work?

Contribute to the Tax Foundation

Share This Article!

Let us know how we can better serve you!

We work hard to make our analysis as useful as possible. Would you consider telling us more about how we can do better?