Products You May Like

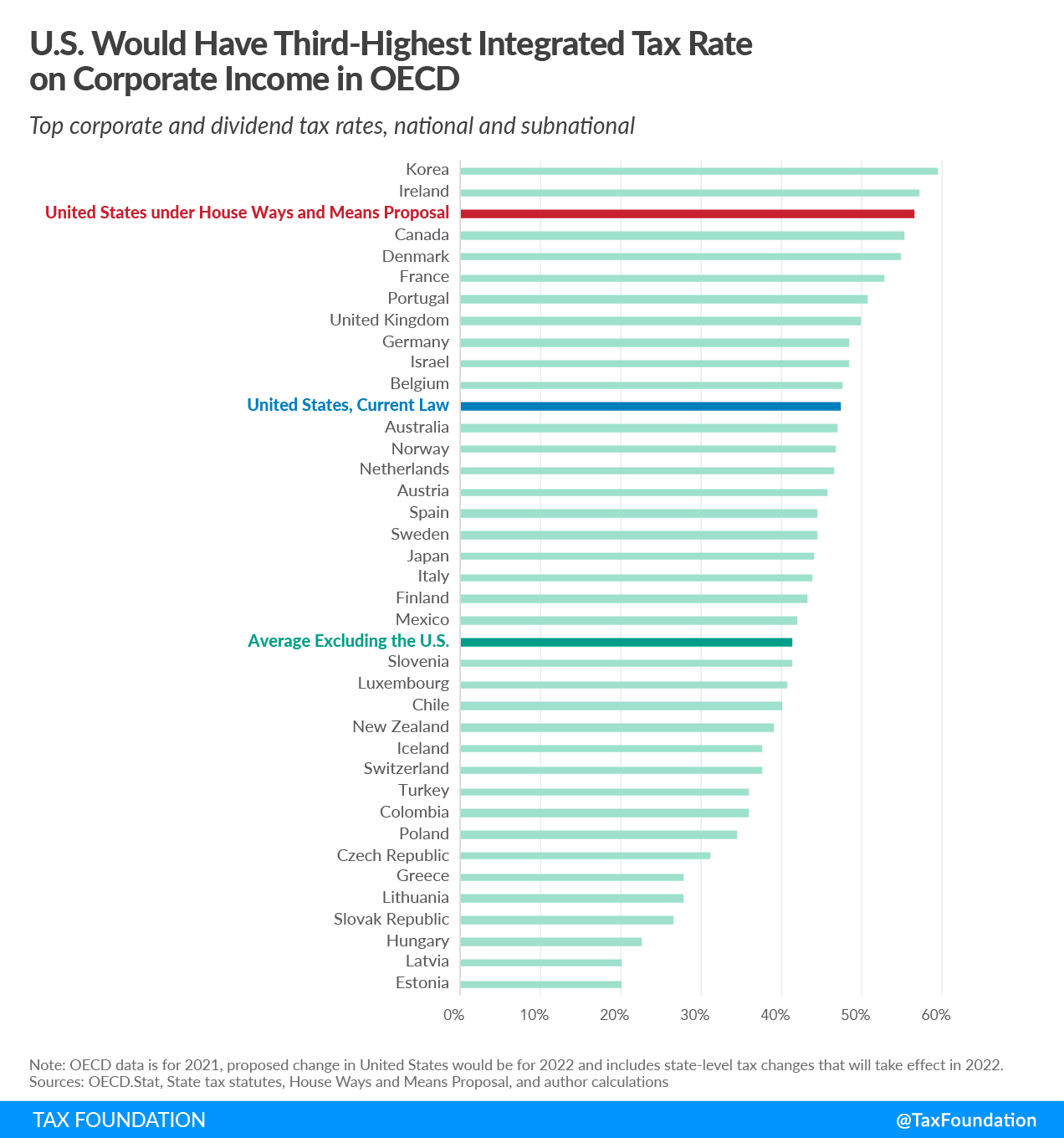

Under the House Ways and Means plan to raise taxes on corporations and individuals, the integrated tax rate on corporate income would increase from 47.4 percent to 56.6 percent—the third highest in the OECD. To reduce this burden, policymakers could explore integrating the individual and corporate tax systems. Several developed countries have done this to reduce or completely eliminate the double taxation of corporate income.

The U.S. imposes taxes on two kinds of business forms. Pass-through business, such as sole proprietorships, partnerships, and S corps, pay taxes through the individual income tax code. However, C corporations face two layers of taxation: one at the entity level and then another at the shareholder level as a capital gain or dividend. The double taxation of corporate income reduces investment and distorts business decisions. Specifically, businesses are more likely to borrow money to finance projects, due to tax preferences given to debt financing, or organize their business as a pass-through entity to reduce their tax burden.

The U.S. reduces this double taxation of corporate income by taxing long-term capital gains and qualified dividends at lower rates, under what is known as a “modified classical system.” The U.S. is among seven OECD countries that taxes corporate income this way. However, even when accounting for this preferential treatment, the U.S. continues to impose among the highest top marginal tax rates on capital gains and dividend income. Under current law, when accounting for federal and average state taxes, the U.S imposes an average combined tax rate of about 29 percent on capitals gains and dividend income, higher than the OECD average of 23.9 percent on capital gains and 19.1 percent on dividend income. The House Ways and Means plan would increase the combined tax rate on capital gains and dividends to about 37 percent, the third highest in the OECD.

Due to these high top marginal rates, the two layers of taxation create a significant tax burden on corporate income. Imagine a corporation that earns $100 in profit. Under the House Ways and Means plan, the business would be pay $30.92 in corporate taxes (a combined federal and state tax rate of 30.9 percent), leaving the corporation with $69.08 in after-tax profits. When these earnings are distributed to shareholders as dividends, the income would be taxed again at the individual level. The shareholder would pay $25.67 in income taxes (a combined federal and state rate of 37.2 percent). Total after-tax income would fall to $43.41, resulting in a combined marginal tax rate of 56.6 percent on corporate profits.

| Integrated Tax Rate Under Current Law | Integrated Tax Rate Under House Ways and Means Plan | |

|---|---|---|

| A. Corporate Profits | $100.00 | $100.00 |

| B. Combined Corporate Income Tax | $25.75 | $30.92 |

| C. Distributed Dividend (A-B) | $74.25 | $69.08 |

| D. Combined Dividend Income Tax | $21.67 | $25.67 |

| E. Total After Tax Income (C-D) | $52.58 | $43.41 |

| Integrated Tax Rate (A-E) / A | 47.4% | 56.6% |

|

Note: Proposed change in United States would be for 2022 and includes state-level tax changes that will take effect in 2022. Sources: State tax statutes; House Ways and Means proposal; and author calculations. |

||

The same double taxation occurs even if the corporation retains its after-tax earnings, rather than distributing them as dividends. When corporate earnings are retained, the value of the stock rises to reflect an increase in assets held by the corporation. Shareholders that decide to sell their stock will realize a capital gain and pay a tax on that gain. In the above example, the capital gain would face a tax rate similar to that on qualified dividends, about 37 percent.

The double taxation of corporate profits creates a number of distortions in the economy. Two layers of taxation on corporate income increases the cost of capital. When a corporation decides whether to invest in a new project, it needs to make sure its after-tax return on the project is high enough to satisfy investors. If the return is too low, the corporation won’t pursue the investment. All things being equal, a higher cost of capital makes it less likely that corporations will invest in projects. This leads to lower levels of investment and a smaller capital stock in the overall economy. A smaller capital stock means lower worker productivity, lower wages, and slower economic growth.

The double tax on corporate income also distorts the organizational form of businesses. Unlike traditional C corporations, pass-through businesses only face one layer of tax: when the income is reported on the individual tax returns of the owners. Under current law, the top federal marginal tax rate on pass-through business income (45.9 percent) is lower than the integrated rate on corporate income (47.4 percent). Certain pass-through businesses may also deduct up to 20 percent of their qualified business income from their taxable income under Section 199A of the tax code, further reducing their tax burden.

Due to the tax differential between the two forms, businesses have an incentive to forgo the benefits of incorporation in order to receive a higher rate of return on investments. Since 1986, when individual income tax rates sharply declined relative to corporate tax rates, more and more business income has been reported by pass-through businesses. In 1980, pass-through businesses only accounted for roughly 30 percent of total business income. As of 2015, pass-through businesses earned 62 percent of all business income.

Double taxation is partially limited through interest deductibility in the tax code. Corporations that finance their investments with debt, rather than equity, are able to deduct interest payments made to lenders. This passes the pretax earnings to lenders in the form of interest, who then pay only one layer of tax on that income. Due to the preferences given to debt over equity in the tax code, corporations may have an incentive to borrow more than they otherwise would in the absence of double taxation on equity investment.

The 2017 tax reform limited interest deductibility to 30 percent of earnings before interest, taxes, depreciation, and amortization (EBITDA), which is scheduled to be limited further to earnings before interest and taxes (EBIT), starting in 2022. The House bill proposes an additional limitation on net interest expense for U.S. multinational corporations. These changes reduce the debt bias by applying double taxation to debt and equity.

Fundamental tax reform would eliminate the double taxation of corporate income. Short of reforming the entire tax code, there are options to reduce double taxation by more fully integrating the individual and corporate tax codes, as many other countries have done.

Australia integrates its corporate and individual income tax with a tax credit imputation. This method of integration is a system by which the corporation and the shareholder both pay part of the corporate income tax, but the shareholder is given a tax credit to offset the taxes already paid by the corporation. In the end, corporate income is taxed at the marginal income tax rate of its shareholders, whether the shareholder has a higher or lower tax rate than the corporation. In the U.S. context, this system has the advantage that it would treat pass-throughs and traditional C corporations roughly equally–all business income would be taxed at the pass-through rate. Including Australia, nine OECD countries have full or partial credit imputation systems (Table 2).

Estonia integrates its corporate and individual income tax by having a full dividend exemption at the shareholder level. This system of integration levies only one layer of tax at the corporate level on distributed corporate income. When an Estonian corporation makes a profit and distributes it to shareholders, it must pay the corporate income tax of 21 percent, or $21 on $100 of profit. When a shareholder receives the after-tax profits of $79, no additional tax is due. The total tax on distributed profits between the corporation and the individual is 21 percent. Including Estonia, six OECD countries have full or partial dividend exemptions (Table 2).

| Classical System | Modified Classical System | Credit Imputation | Dividend Exemption | Other |

|---|---|---|---|---|

| Austria | Denmark | Australia | Estonia | Hungary |

| Belgium | Greece | Canada | Finland | Norway |

| Czech Republic | Poland | Chile | France | |

| Germany | Portugal | Colombia | Latvia | |

| Iceland | Spain | Japan | Luxembourg | |

| Ireland | Switzerland | Korea | Turkey | |

| Israel | United States | Mexico | ||

| Italy | New Zealand | |||

| Lithuania | United Kingdom | |||

| Netherlands | ||||

| Slovak Republic | ||||

| Slovenia | ||||

| Spain | ||||

| Sweden | ||||

|

Source: OECD Tax Database, Table II.4. |

||||

The U.S., like many other OECD countries, mitigates the double taxation of corporate income by taxing capital gains and dividends at reduced rates or exempting a portion of shareholder income from full taxation. The United States is among the 22 OECD countries that taxes capital gains at reduced tax rates. Capital gains that are held for longer than a year are taxed at a top rate of 20 percent, while capital gains held for less than a year are taxed at ordinary income rates.

Twelve countries either partially or fully exempt capital gains from individual-level taxation, which eliminates the double taxation of retained earnings. For example, Australia and Canada provide a 50 percent deduction (50 percent of a capital gain is tax exempt) for capital gain income, while New Zealand does not tax capital gains at all. Estonia, uniquely, exempts retained earnings at the corporate level, but taxes capital gains at the individual level as ordinary income.

Preferential tax rates on capital gains and dividends are not an accident, or a loophole. They serve to reduce the double taxation of corporate income, which is subject to both corporate and shareholder taxes. Double taxation creates a significant tax burden on corporate income, which increases the cost of investment, encourages a shift from the traditional C corporate form, and incentivizes debt financing. These problems would be exacerbated by the proposed tax increases on corporations, shareholders, and lenders. A better solution is to seriously consider integrating the corporate and individual tax codes, the way many other developed countries have done.